A British Conservative proposes the worst idea in competition policy yet

When you get the facts and the theory wrong, bad policy conclusions are likely to follow.

This week’s newsletter is an edited version of a post that originally appeared on Truth on the Market, a website full of scholarly commentary on law, economics, and more.

UK Member of Parliament (former Conservative Party Cabinet Minister) Kit Malthouse published an essay in CapX earlier this month titled “We need a competition revolution.” I, of course, completely agree that competition is vitally important to any economy, and the UK has been struggling with productivity and growth challenges that may be linked to competition issues. As an American observer, I’ve had the impression that the UK Conservatives were the economically sensible party. But apparently not.

As I read Malthouse's piece, I found myself increasingly disillusioned.

Rather than an evidence-based, market-oriented approach I expected from a Conservative, Malthouse paints a dire picture of rampant monopolization across British industries: “we see the same pattern: a handful of dominant firms controlling vast swathes of the economy, shutting out competition and stifling innovation.”

Malthouse’s argument suffers from two fundamental problems: it is wrong on the evidence, and it is wrong on the economy theory. Besides that, it is not a bad piece.

On Market Concentration

Malthouse’s fundamental claim about growing market concentration simply doesn’t align with the evidence. The best summary comes from a recent report from the UK’s Competition and Markets Authority (CMA), which shows that the Herfindahl-Hirschman Index (HHI), the most comprehensive measure of market concentration, has barely changed over the last 25 years. It increased slightly from around 1,100 in 1997 to 1,300 during its peak, before falling back to just above 1,100 by 2022.

The timing matters: “Across a range of measures, concentration increased during the mid-late 2000s, then fell slightly. The latest data (2022) shows that it stands at similar levels to 1997.” The dates are worth noting, as the UK productivity slowdown (as in the United States) started around 2006. Thus, concentration has been falling during the productivity slowdown that is plaguing the country. That should be a big flashing sign of the need to dig deeper.

The mean-concentration ratio of the top five UK firms only increased from 43% to 47% over the last quarter century—hardly the dramatic consolidation that Malthouse describes. This completely undermines his narrative of a recent, worsening crisis with monopolies “controlling vast swathes of the economy.”

You could say that 43% was still problematic, and the economy suffered from the same problem in 1997. Unfortunately, that would mean that none of Malthouse’s explanations work. His entire essay frames market concentration as a recent and worsening crisis; he talks of monopolies “controlling vast swathes of the economy” and using present-progressive language like “we are seeing the emergence of near-monopolies.” He specifically claims the Conservative Party “allowed ourselves to be seduced by big business” in recent decades, that “competition is being throttled,” and his rhetoric about competition policy having “lost our way” all paint this as a recent deterioration. Yet if concentration levels in 2022 are virtually identical to 1997, then this narrative of recent capture by “corporate titans” and his historical arc of declining competition collapses. The problem either existed in the late 1990s (negating his claims about recent regulatory failure) or doesn’t exist now to the degree he claims at all.

Business Dynamism: A Real Concern, but Mischaracterized

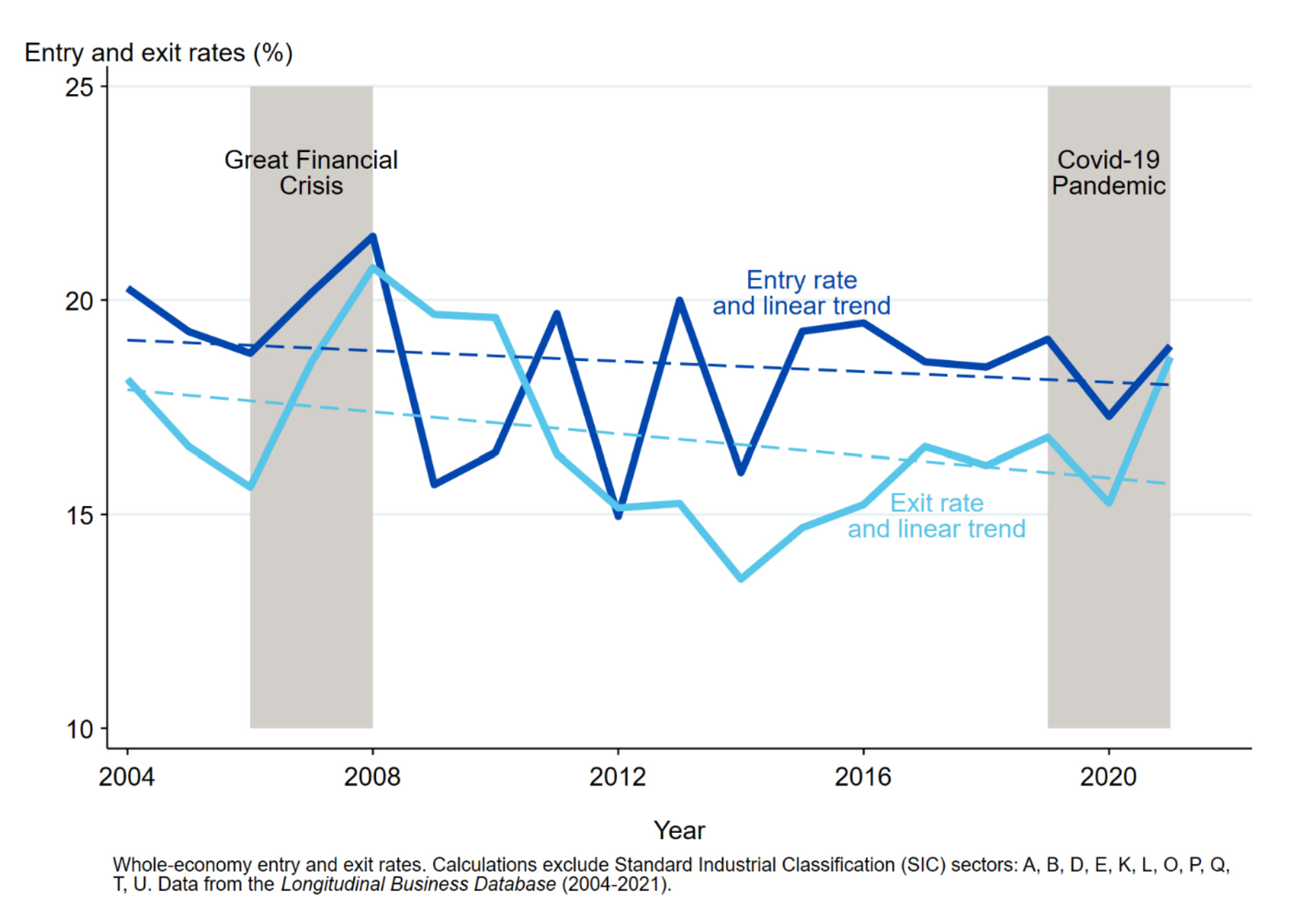

Malthouse touches on a genuine concern about declining business dynamism that’s supported by the evidence. Market entry rates declined from around 14% in 2004 to about 11% by 2021, while exit rates fell from approximately 11% to 10%. The job-reallocation rate declined from about 32% in 2004 to roughly 24% by 2021, and the employment share of young establishments (under five years old) fell dramatically from 40% to 20%.

The report also shows increased persistence of top firms in every major sector of the economy, with firms that have the highest markups increasingly maintaining their position over time. Persistence in the top 10% of markup distribution has increased from around 24% to 29%. This suggests reduced competitive pressure on incumbent firms.

Malthouse’s characterization of the economy as “increasingly defined by minnows and whales—giant conglomerates at one end and struggling startups at the other, with almost nothing in between” does find some support in young firms’ declining shares in employment and turnover. His concern about mid-sized businesses being “either swallowed up by larger firms or driven to collapse or emigration before they can scale” aligns with some of the evidence on reduced dynamism.

But Malthouse’s diagnosis of why this is happening—primarily due to monopolistic behavior—doesn’t necessarily follow from the data. That conclusion simply ignores much more important factors: technological changes, shifting consumer preferences, and structural economic transformations. We can see this, because the industries affected aren’t all the same.

While Malthouse correctly notes that markups have risen, his explanation for this trend doesn’t match the evidence. He suggests this is primarily due to monopolistic exploitation, but the report finds “the technology explanation plays a more significant role in driving markup trends in the UK” than anti-competitive conduct.

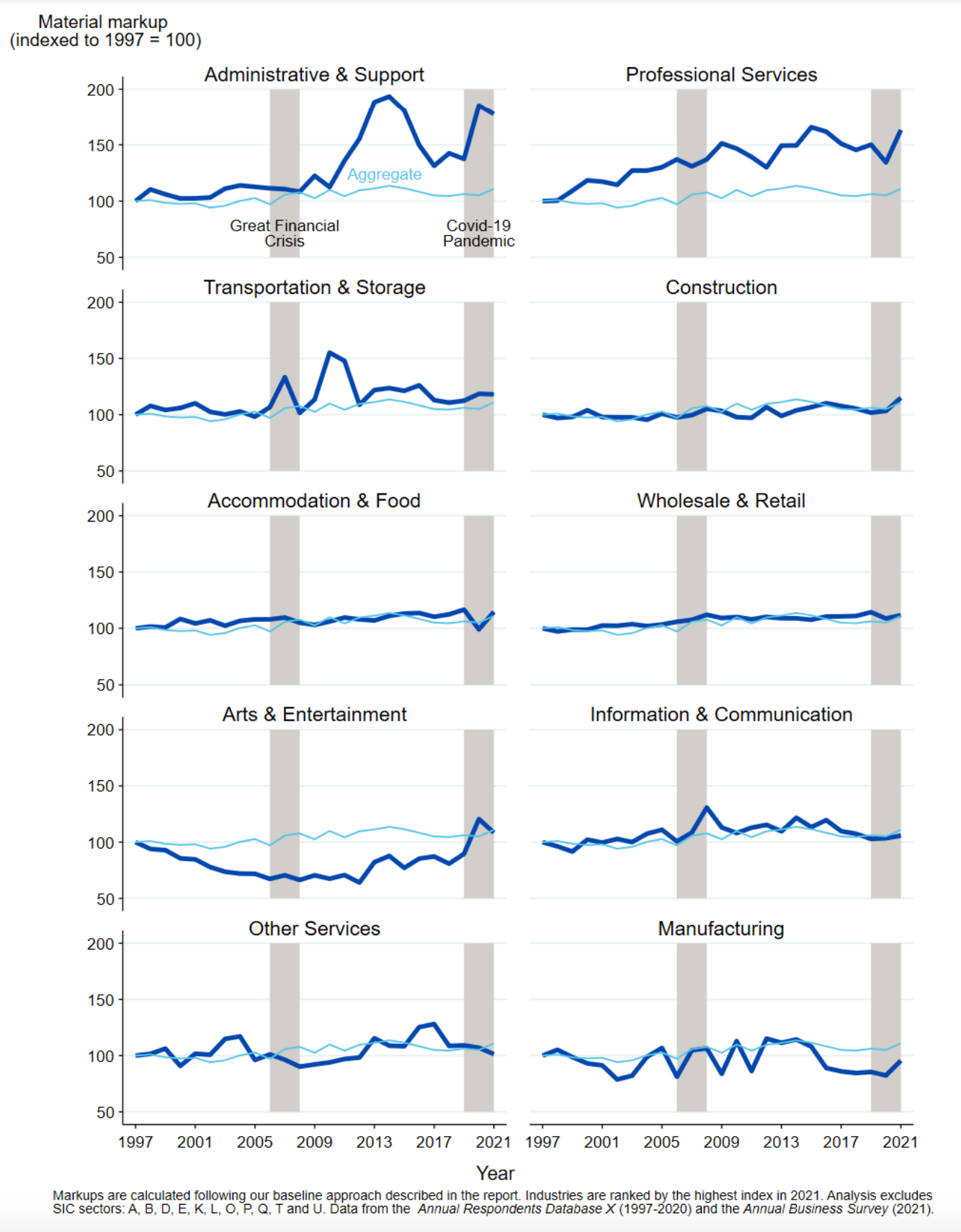

The report shows significant sectoral variation in markup trends. Administrative and support services, professional/technical/scientific services, and arts and entertainment have seen rapidly rising markups. In contrast, manufacturing, construction, and accommodation/food services have experienced milder increases.

Crucially, the report reveals that markup increases have been “driven predominantly by firms that already have the largest markups” and that “the dispersion of markups has grown,” both of which indicate widening gaps between market leaders and followers. This suggests that certain firms may be pulling ahead not just through market power, but through superior technology, productivity, or business models—factors that might actually benefit consumers through better products and services.

The CMA’s finding that technology plays a more significant role than anti-competitive conduct in driving markup trends directly contradicts Malthouse’s narrative of monopolistic exploitation as the primary driver. This doesn’t mean that rising markups aren’t concerning, but it does suggest that Malthouse hasn’t seriously considered other factors. In the United States, technology seems to be the main driver, so that’d be a good starting point for the UK.

The Industries Don’t Match

Perhaps most tellingly, Malthouse focuses heavily on banking, energy, telecoms, and supermarkets as his primary examples of problematic monopolies. An entirely different set of sectors, however, have the highest markups and greatest competition concerns.

The CMA report ranks different industry clusters across a variety of measures of competition, such as markups and concentration. This heatmap visualizes a comprehensive assessment of competition across different sectors of the UK economy. An industry cluster that is ranked most competitive along one dimension is just as likely to be least competitive along another.

The four industries with the most concerning markup levels are “creative arts and entertainment; temporary employment activities; information services; and the organisation of conventions and trade shows.” None of these feature prominently in Malthouse’s critique besides information services (and even there, he paints tech as primarily a U.S. problem).

Manufacturing, which he suggests is dominated by monopolies, has actually seen stable markups over the last 25 years. His dynamism narrative is similarly misplaced. Contrary to his claims about these sectors, transportation/storage and wholesale/retail have actually experienced growing business dynamism.

In a paper on the United States that I co-authored with Ryan Decker, we show that the industries experiencing larger increases in markups actually saw less of a decline in dynamism. The CMA replicated our baseline analysis for the UK and found the same thing: industries with the highest markups “neither have particularly high nor increasing concentration.” Even more, “several industry clusters with high markups nonetheless feature high productivity, investment, and business dynamism”—a finding that is directly in line with our US results.

When you plot the industry markup against different measures of dynamism, higher markups correlate with higher dynamism, exactly opposite what Malthouse would suggest.

Again, we have a complete mismatch between Malthouse’s focus and the actual evidence, which suggests his critique may be based more on perception than on evidence.

On Regulatory Capture

Malthouse reserves particular disdain for what he sees as toothless regulators who have been captured by industry. He writes that: “Nothing illustrates the jaw-dropping failure of regulation more starkly than the appointment of Doug Gurr, a former Amazon executive, as the interim chair of the Competition and Markets Authority (CMA).” He calls this “the very definition of regulatory capture: a regulator that no longer regulates but facilitates.”

Yet the CMA report itself contains no evidence of declining enforcement. In fact, it suggests that UK merger control may have been more effective than U.S. enforcement in preventing the accumulation of market power. The report notes that:

In contrast to the US, where studies have shown that M&A activity has materially contributed to rising markups, there is no evidence in the UK to indicate that markups have been driven by M&A activity, or ineffective competition enforcement.

The report shows that enforcement activities have remained relatively steady across various tools over the past decade. Phase 1 and Phase 2 merger investigations have remained consistent, with a slight increase in Phase 2 cases, which typically address more problematic mergers. While Malthouse claims that the “watchdogs have become lapdogs, and big businesses spend more time and money influencing regulators than innovating,” the data simply don’t support this narrative of declining enforcement.

The Worst Antirust Idea?

Malthouse’s most alarming proposal is his automatic-breakup investigation threshold: “If a firm controls more than 50% of a market, a breakup review should be triggered automatically,” with “the burden of proof...on the company to prove it is not behaving anti-competitively.”

This idea reveals a fundamental misunderstanding of how markets work and would create catastrophic incentives throughout the economy. Let’s examine why.

First, the 50% threshold is completely arbitrary. Many markets naturally tend toward higher concentration due to economies of scale, network effects, or other efficiencies that benefit consumers. In industries with high fixed costs and low marginal costs—like software, pharmaceuticals, or telecommunications—larger firms can offer products at lower prices. Breaking them up would eliminate these efficiencies and likely raise prices for consumers.

Second, this arbitrary line-drawing demonstrates the fundamental problem with automatic-review thresholds. A company like Whole Foods would face constant uncertainty about whether they're approaching a dangerous threshold. Are they competing in “premium organic groceries” (where they would exceed 50%) or “all groceries” (where they wouldn’t)? The answer depends entirely on how a regulator chooses to define the market — something the business cannot control or reliably predict. This definitional gerrymandering means well-run companies must constantly worry about growing too successful in whatever sub-market a regulator might carve out. The uncertainty alone would chill investment and innovation. Why develop a revolutionary product if success might trigger a costly breakup review?

Third, and perhaps most damaging, this policy would create perverse incentives that would actively harm consumers. Companies approaching the 50% threshold would face a stark choice: either deliberately limit growth, raise prices to reduce market share, or face a costly breakup process. This would lead to several destructive outcomes:

Companies would deliberately restrict output and raise prices as they approach 50% market share to avoid triggering the review.

Firms would stop investing in improvements that might attract more customers once they near the threshold.

Innovative companies would be punished for creating products that consumers prefer. If a company gains market share by offering a superior product at a better price, why should they be penalized?

Firms might engage in wasteful activities or artificial inefficiencies just to stay below the threshold.

Consider a concrete example: When Apple introduced the iPad in 2010, it instantly captured over 75% of the tablet market. This dominance wasn't achieved through anti-competitive behavior but by creating an innovative product that consumers loved. Under Malthouse’s proposal, Apple would have faced an automatic breakup review simply for its success.

To avoid this, Apple might have deliberately limited production, kept prices artificially high, or stopped improving the iPad—all outcomes that would have harmed consumers. Furthermore, Apple's market leadership in tablets spurred competition, with companies like Samsung and Microsoft developing their own—ultimately expanding consumer choice. Malthouse's policy would have potentially stifled this entire category of innovation. The same logic applies to numerous other successful innovations where the innovator wins a large share of the market.

Even more extreme, if a company is really innovative, they will create a whole new market where they start with 100% of the market. Should every innovator have the threat of breakup hanging over them with a presumption of guilt?

The 50% threshold is even more destructive when paired with other ideas Malthouse has put forward. For example, his suggestion that “a dominant player with more than 50% who lowers their prices to gain market share should ring alarm bells” is especially troubling. He’s essentially arguing that lower prices—the very outcome that competition policy is supposed to encourage—should be illegal. What this will do is give companies in this position a good reason not to cut prices, and make it riskier for them to do so.

This gets the entire purpose of competition policy backward. We want firms to compete on price and quality; punishing them for successfully doing so undermines the very foundations of market competition.

Malthouse’s Faulty Understanding of Competition

Malthouse’s argument rests on a fundamentally flawed understanding of how competition, concentration, and market outcomes relate to one another. He assumes a simplistic narrative where increased concentration inevitably leads to reduced competition, higher markups, and less innovation. This represents a misreading of modern economic evidence and theory.

The core flaw in Malthouse’s thinking is his assumption that concentration and competition exist on a simple sliding scale—that high concentration means low competition, and low concentration means high competition. This overly simplistic view ignores decades of economic research showing that the relationship between these factors is far more complex, and often counterintuitive.

As I’ve written before, there’s substantial empirical evidence that enhanced competition can actually increase market concentration by letting the best companies win their rivals’ market share. This completely contradicts Malthouse’s core assumption.

The evidence from a huge literature in trade and industrial organization shows that “competition increases concentration” is a common empirical finding. Chad Syverson, a leading economist in this area, explains: “Many empirical studies in varied settings have found that greater substitutability/competition—resulting from, say, reductions in trade, transport, or search costs—shifts activity away from smaller, higher-cost producers and toward larger, lower-cost producers.” Syverson adds that “it is not an exaggeration to say that there are scores, perhaps hundreds, of such studies.”

Concentration is worse than just a noisy measure of market power. We don’t know which way the measure is pointing.

Why does this happen? When competition intensifies—for example, when search costs decrease or products become more substitutable—consumers can more easily switch between providers. This forces companies to compete more aggressively on price and quality. In such environments, the most efficient and innovative firms gain market share, while less productive firms lose ground or exit entirely. The result is often increased concentration, as market share flows to the most capable providers.

Compare the concentration measures between a world with a bunch of isolated towns with one retailer and a world where everyone can buy from Amazon. The pre-internet world of many local monopolies would register as having low overall concentration (many small firms across the country), while today’s world of e-commerce might appear more concentrated. Yet today’s consumers clearly benefit from more choice, lower prices, and greater convenience—all hallmarks of increased, not decreased, competition.

This also explains why Malthouse’s examples don’t align with the empirical estimates of problematic sectors. The industries he focuses on (banking, energy, telecoms, supermarkets) aren’t the ones showing concerning patterns of concentration. The sectors that actually display concerning metrics (creative arts and entertainment, temporary employment activities, information services, conventions and trade shows) get little attention in his essay.

Additionally, Malthouse fails to understand that concentration can increase for beneficial reasons. When a company develops superior products, more efficient processes, or better customer service, it naturally gains market share. This process of “creative destruction,” whereby better firms replace worse ones, is precisely how markets are supposed to work. A new, very efficient upstart will initially decrease concentration before winning over a large portion of the market and increasing concentration.

By treating all concentration as suspicious, Malthouse’s proposed 50% threshold for automatic-breakup reviews would actively punish companies for succeeding through superior products or efficiency. This would create perverse incentives where firms approaching the threshold might deliberately raise prices, reduce quality, or stop innovating to avoid triggering a breakup review.

While it’s encouraging to see a senior MP like Kit Malthouse taking an interest in competition policy, this essay reveals a profound disconnect between political rhetoric and economic reality. His proposals demonstrate a concerning lack of understanding of market dynamics, competition theory, and empirical evidence.

This approach to economic policymaking helps explain the UK’s disappointing economic performance over the fourteen years of Conservative governance. Britain deserves competition policies grounded in sound economic understanding—policies that would foster innovation and growth, rather than stifle them under misguided regulatory burdens.

One can only hope that future policy discussions will be informed by a more sophisticated understanding of how markets actually work. The UK’s economic future depends on it.

How many market participants are required to assure competition?

One.

How much policy is required to assure optimum competition?

None.

I hadn't heard about this MP's proposal, but this article just reinforces the view I have held for some time, that we need to raise politicians' wages to Singaporean levels because we are stuck in a pay-peanuts-and-get-monkeys vicious circle.