A simple approach to dynamic mergers

Can we capture the core trade-off without going full IO?

Two rocket companies combined to form a de facto monopoly. It was probably a good idea 🤷♂️

So, a little context. In 2006, Boeing and Lockheed Martin combined their launch divisions in a joint venture into United Launch Alliance. That’s what I mean when I say they combined. It’s not actually a merger, and there are important differences when you get into the weeds of antitrust, but let’s think of this as a merger to a monopoly for simplicity. This seems bad and extra bad in an industry that handles national security payloads.

By every static measure, this is the textbook nightmare.

Economic Forces readers will know I think the textbook metrics are a bad starting point. So I was intrigued to see a recent paper by Ruibing Su, Chenyu Yang, and Andrew Sweeting, which argues it was probably a good idea.

Their key mechanism that is missing from the basic model is that every launch teaches you something. The engineers who fly the fiftieth mission know things the engineers on the first mission didn’t. And before the “merger,” that asset was being duplicated across two separate programs with separate engineering teams, separate supply chains, separate everything. So we have a clear possibility (not sure if its plausible yet) for an efficiency in a specific sense.

Is that efficiency enough to outweigh the standard monopoly problem?

Su, Yang, and Sweeting argue yes. They use a full structural model, lots of bells and whistles, modern industrial organization stuff. They look at the space launch industry from 1985 to 2024 and argue the learning synergies were real and large enough to outweigh the market power. They also find that when the government committed to multi-year block buys rather than shopping launch by launch, costs fell dramatically. Forward-looking procurement gave the supplier incentive to invest in getting better, even without a competitor pushing them.

That’s a serious empirical study for one industry. The harder question is what regulators were supposed to do at the time.

We usually punt on dynamics

Every merger in a learning-intensive industry raises the same questions. Will the merged firm keep innovating, or get comfortable? What happens to entry when the incumbent has a decade of accumulated know-how and the challenger starts from scratch? Will the firm use its position to lock up inputs and foreclose rivals?

In practice, regulators mostly punt. They evaluate mergers on the static margin and treat “dynamic efficiencies” as a vague thing out in the ether, too speculative to count for much. That bias always cuts the same way. It cuts against mergers in the industries where dynamic effects are biggest.

It’s fair. Studying dynamic efficiency is hard. Full dynamic models can deliver answers, but the people who build them admit they come with lots of costs. Doraszelski and Pakes in their handbook chapter on “Applied Dynamic Analysis in IO” caution the framework “delivers very little in the way of analytic results of applied interest.” Berry and Compiani, in another summary of the dynamic literature, aren’t really any more positive. “[T]he attempt to add dynamics may create enough compromises that the result is not better than the static model.”

So, yeah, if the only way to engage with dynamics is a five-year structural project, most merger reviews will keep ignoring them.

Turning static to dynamic to static

Let’s work through some other options. Instead of going full structural IO, let’s think in simple price theory times. Strip away the details. I think there’s a simple way to capture a lot of the interesting dynamics here.

The key idea here is that output today affects costs tomorrow. The firm that produces more accumulates something.

That’s a reduced form way of capturing lots of different things. The learning-by-doing example of rockets makes sense, but it’s only one case. Retailers do the same thing with distribution density. Airlines do it with routes. A manufacturer that keeps producing refines its tooling and supplier relationships in ways a competitor running smaller volumes can’t match. The platform version is an installed base.

The engineering details differ. Don’t let that obstruct things. The economics is the same. Output today builds a productive stock, and that stock lowers future cost.

Notice this is not standard capital accumulation. That is a separate decision that sort of fights with production. Cash spent on a new machine is cash not spent directly making product. Time spent building the next semiconductor line is time not spent producing the current one. In your basic dynamic model with capital accumulation, production and investment compete for the same scarce resources in a more direct way.

The productive stock here works differently. You can’t write a check for a year of launch experience or a denser route map. The only way to build it is to produce. So output and investment don’t compete. They’re the same decision. Producing more today is investing more today.

Circling back to mergers in particular, of course, this doesn’t cover every dynamic merger claim. Some dynamics are about patent races, product repositioning, entry timing, demand-side network effects, or strategic investment chosen separately from output. Those may require different tools.

But most merger-efficiency claims are more mundane. They’re about scale, experience, density, know-how or having some installed base. For example, when T-Mobile and Sprint argued in 2019 that combining their spectrum holdings and cell sites would let them build a higher-quality 5G network than either could alone, that’s a network-density claim. The “stock” is network capacity. Producing more output builds that.

Always some tradeoffs

A merger with this type of capital does two things at once, pulling in opposite directions.

Of course, we still have the standard worry of the drop in competition. The new firm doesn’t worry about product diversion. If Boeing’s launch business raises price before common control, some lost business goes to Lockheed. After common control, those sales stay inside the same organization. The combined organization recaptures customers it used to lose. That weakens the incentive to fight for the marginal customer, which means higher markups and less output.

We can draw this out. Common control rotates the marginal benefit curve in. Before the combination, winning a launch from your rival is a gain. After the combination, winning a launch from your other division is partly stealing from yourself. The combined firm internalizes cross-product diversion, so the marginal benefit of expanding output is lower. Quantity falls.

That’s the normal merger logic.

But here we have a competing force. If producing today builds capability for tomorrow, each extra launch is also a little more experience and operating capability. That lowers the effective marginal cost of producing today. When the effect is large enough, the supply curve slopes down. The firm is paying the current cost of the launch, but it is also buying future cost reductions.

If consolidation means the combined organization captures a larger share of the returns from building productive capability, it has a stronger incentive to produce today. Combined production volumes mean faster learning. More internal coordination means the cost savings actually show up rather than getting duplicated across separate programs.

Draw the picture

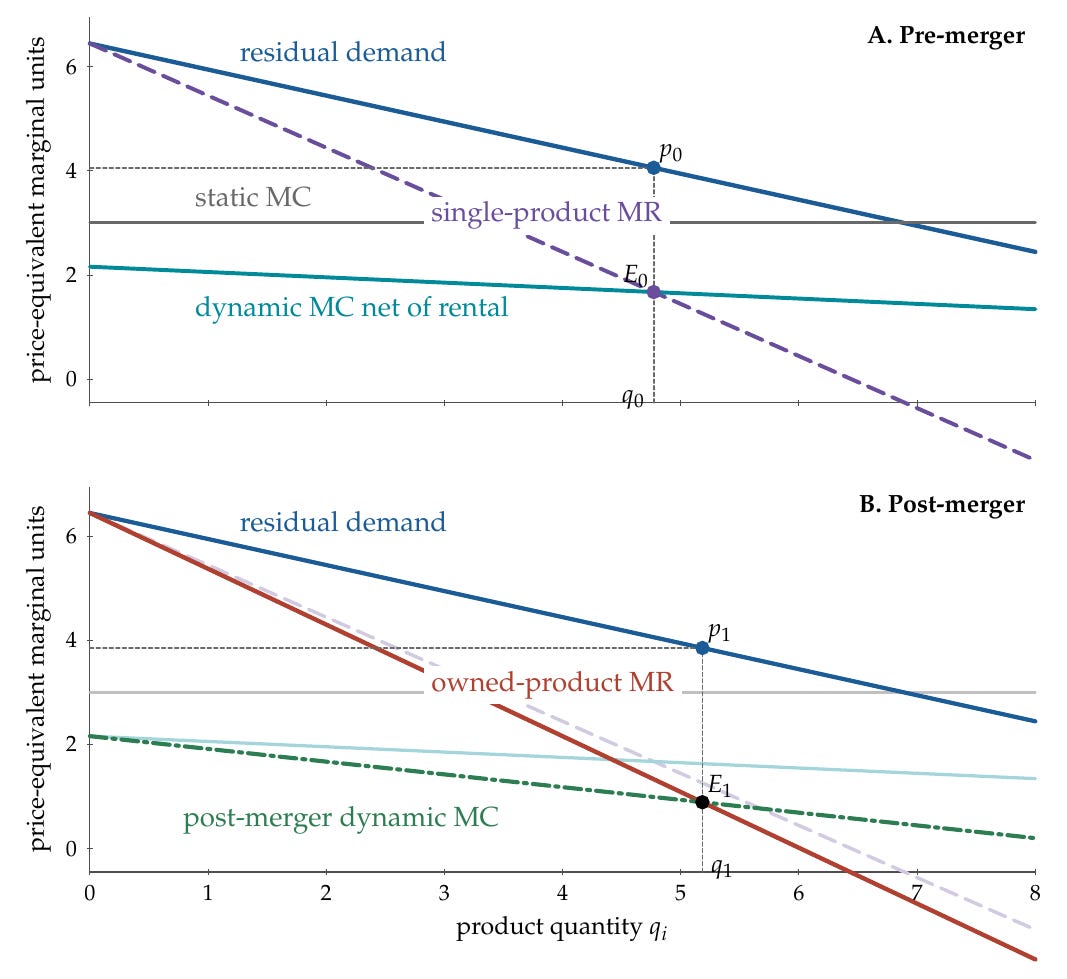

To see the two forces in one picture, we need to think about the marginal cost of this productive stock. How does it change the marginal cost curve? What’s the price?

Capital has a rental rate, what you’d pay per period to use it. Jorgenson called it the user cost of capital; it’s the implicit rental on an asset the firm owns rather than rents. We can think of experience and operating capability have the same structure, even though no one cuts you a check, just as most firms own their capital so don’t pay a rental/user cost.

What’s the value of owning that capital? Each unit of output today adds to the stock and lowers tomorrow’s cost. The present value of that future saving is the implicit rental rate on the stock. Producing one more launch is cheaper than the accounting cost suggests, because part of what you pay “buys” future productivity.

Call the normal accounting cost per launch the static marginal cost. Call the static cost minus the rental rebate the dynamic marginal cost “net of rental”. Static MC is what shows up on the invoice. Dynamic MC is what actually drives the firm’s output decision once it values the stock.

Pre-merger, in the top panel, the firm faces residual demand for its own product and a single-product marginal revenue curve. Static MC sits at 3. Dynamic MC, net of the rental rebate, sits closer to 2. The firm produces where MR meets dynamic MC. We can read off the price and quantity.

Post-merger, two things change at once. MR rotates inward to “owned-product MR.” This is the standard diversion effect in picture form. If that was all that happened, mechanically, the merger would reduce output and raise prices.

Here, second force is that the dynamic MC rotates further down to “post-merger dynamic MC.” The combined firm captures more of the rental value of producing today. Less duplication across two engineering organizations. Higher combined volume moving up a learning curve (or moving down the cost curve). More of the future cost reduction stays inside the firm rather than leaking to a competitor. The rebate gets bigger, so the firm’s perceived marginal cost falls.

In the figure, the dynamic-MC shift dominates.

The picture also tells you when the result flips. If the learning curve is flat, dynamic MC barely moves and the MR rotation wins. Quantity falls, price rises, cats and dogs, living together, mass hysteria.

In some sense, this is all trivial. If the force that pushes up quantity is greater than the force that pushes down quantity, quantity goes up. Not exactly a deep insight. The figure can help us think through when the result flips.

But we can think even more about how learning works and how that maps to the figure. If experience spills over to competitors, the merger doesn’t change how much of the rebate the firm captures, and again dynamic MC barely changes. The industry already has that downward sloping curve, even if each firm doesn’t. Which one dominates depends on the slope of learning, how private it is, and how durable. The theory can guide your investigation into these questions.

Then we can start thinking about alternatives. A merger is one way to change the return to producing today. It is not the only way. Su, Yang, and Sweeting find that when the government switched from buying launches one at a time to committing to multi-year block buys, which is a way of guaranteeing the supplier a stream of future orders, costs fell sharply. The mechanism is the same one the figure shows. A bigger committed order book raises the value of investing in learning today, because the firm knows it will be producing the launches that benefit from that learning. The rental rebate gets bigger. Dynamic MC rotates down.

Is the stock the harm?

The figure shows when a merger generates real cost savings: steep learning curve, private experience, durable stock.

We need to be careful here. Those same parameters make entry hard. A new entrant starts at zero experience while the merged firm sits on years of accumulated know-how. If learning is steep, the cost gap is large. If learning is private, the entrant can’t catch up by hiring engineers away. If the stock is durable, the gap persists.

It’s tempting to call the entry barrier the offsetting cost of the efficiency and try to net them out. I’ve argued before that this gets the analysis wrong. Achieving scale is not an antitrust harm. Preventing a rival from achieving scale through better products or lower prices is not an antitrust harm either. Both are what competition on the merits looks like.

The same goes for an accumulated learning stock. If ULA’s experience makes it harder for an entrant to win contracts, that’s the productive stock doing its job. The merger that built the stock faster did so by combining output, not by doing anything to competitors.

The harm has to be a specific mechanism. The restraint is the harm, not the stock. Foreclosing key inputs. Locking up distribution. These raise rivals’ costs in ways that have nothing to do with the merged firm’s own productivity.

In this case, it turns out ex post that entry was possible and SpaceX completely changed the game and this all seems almost irrelevant. But not every market will have that type of entrant to switch things up.

Again, we have the tools to think carefully through it. This quick analysis doesn’t replace the structural model but gives you a way to think about the question before you build one, and a way to see what the model is doing once it’s built. It forces you to be specific about trade-offs and mechanisms. Which curves are shifting? What’s moving which way? Which ones can you see ex ante, and which ones only show up after the fact? If we can even clearly articulate that, we are a long way toward understanding a market.

So rational firms will intentionally overproduce today—sometimes even selling below current marginal cost—to aggressively slide down the learning curve and capture a cost advantage tomorrow.