Greedflation: Let's Try This Again...

You are reading Economic Forces, a free weekly newsletter on economics, especially price theory, without the politics. Economic Forces arrives weekly in the inboxes of over 8,500 subscribers. You can support our newsletter by sharing this free post or becoming a paid subscriber:

I wrote a post back in February about how price theory can be used as an antidote to bad economic arguments. The argument I was addressing in that post was this notion of “greedflation”, or the belief that rising inflation is caused by higher mark-ups by firms. For those who haven’t been paying attention, the steelman version of the “greedflation” argument is essentially as follows. In the wake of supply chain disruptions, firms faced temporarily higher costs. They used these higher costs to increase prices and that is how we got inflation.

What I pointed out is that the basic price-setting model used in economics suggests this is wrong. The markup of price over marginal cost should get smaller when marginal costs rise. The intuition is simple. When firms face downward-sloping demand curves, they can only pass along a fraction of their increased costs to the consumer. In addition, even if you conjecture that marginal costs rose and then declined, maintaining permanently higher prices for their products would suggest that firms are not profit-maximizing.

In writing that post, I felt in some sense as though I was beating a dead horse. And yet the horse not only lives, it seems to be aggressively fighting back — at least in the world of financial journalism. Let us now try to beat this live horse. But, to make things interesting, I’ll use a separate weapon this time.

Relative Prices and Money Prices

When we reference prices, we always reference money prices. If I ask how much you paid for your loaf of bread, you typically say $3 and not 3 Snickers bars or 0.03 pairs of shoes. Even if you quote me the price in Norwegian kroner, I don’t try to convert that to Snickers bars or pairs of shoes. I convert it to dollars. But economics generally, and price theory specifically, is concerned with relative prices. Admittedly, economists sometimes bungle this message. The reason is that economists like to make an “all else equal” assumption. When doing so, an increase in the relative price of oranges isn’t any different than an increase in the money price of oranges.

This might not seem like an important distinction, but it really is. Whether people realize it or not, every decision that we make is about relative prices. For most readers of this newsletter, if I give you the price of something in dollars, you can probably tell me if that good is expensive or not. You know whether something is expensive because you know what your income is in terms of dollars and you know what other goods cost in terms of dollars. To convince yourself of this, imagine that I tell you that a loaf of bread costs 50 kroner. Could you tell me if the bread is expensive or not? I suspect not without a Google search. (Beklager til mine norsk lesere.)

Nonetheless, a clear understanding of relative prices can actually help us to understand money prices. Consider the following example. Suppose that there are only two goods in the world, oranges and gold. Supply and demand determines the equilibrium prices of these goods. Since there are only two goods, the equilibrium price of oranges in terms of gold in the orange market must be the reciprocal of the price of gold in terms of oranges in the gold market. Otherwise, there would be an opportunity for arbitrage.

Imagine that we are in equilibrium. Someone discovers more gold. Now, at the present price of gold, there is an excess supply. The gold price must fall. This means that one has to give up fewer oranges to get an ounce of gold and one must give up more gold to get one orange.

Notice here that I haven’t mentioned money prices. There is the price of gold in terms of oranges and the price of oranges in terms of gold. But there is no money. One way to introduce money is simply to define it. Suppose that we define our unit of money, one dollar, to be 1/20 of an ounce of gold. This means that by definition the money price of gold is $20 per ounce. By defining the dollar this way, we have not introduced anything that would change the supply and demand for oranges or the supply and demand for gold. Thus, neither the relative price of gold nor the relative price of oranges have changed.

Following the introduction of this unit we are calling a dollar, people start posting prices in terms of dollars. Suppose that once again someone discovers more gold. Again, at the current prices, there is excess supply of gold. This means that the relative price of gold has to decline. The number of oranges that it takes to buy an ounce of gold once again declines.

But, that is about relative prices. What happens to money prices?

The dollar is defined as 1/20 of an ounce of gold. The money price of gold is therefore $20 by definition. The money price cannot change without changing the definition of the dollar. No one is changing the definition of the dollar. So what happens to the dollar price of oranges? The dollar price of oranges must increase. To see why consider that the following is true by definition.

We know that the number of oranges it takes to buy an ounce of gold must decline. This is the same thing as saying that the dollar price of gold must fall relative to the dollar price of oranges. Since the dollar price of gold is fixed, this change in relative prices must occur through an increase in the dollar price of oranges.

The intuition here is quite simple. The only thing that has changed is the supply of gold. There is a lot more gold in the market. Each ounce of gold is therefore less valuable than it used to be. Thus, it takes more gold to buy an orange than it did before. Since the dollar just refers to a certain amount of gold, it necessarily follows that it takes more dollars to buy an orange.

This seems pretty straightforward. Now, let’s extend our analysis to a world with N more goods, where N is an arbitrarily large number. Including gold and oranges, there are now N+2 goods in this economy. However, note that by the same logic we used in the 2-good economy, a gold discovery would have the same effect in this larger economy with more goods. A gold discovery would require that the relative price of gold in terms of every single one of the N+1 other goods would have to decline. For this to occur, since the dollar price of gold is fixed, the dollar price of all these other N+1 goods would have to rise.

This general increase in the dollar price of goods is an increase in the overall price level. All else equal an increase in the supply of gold (and by definition an increase in the supply of dollars) leads to an increase in dollar prices (a rise in the price level). If this was a persistent increase in the gold supply every year, this would mean that dollar prices would rise every year. This persistent increase in dollar prices on average over time is what we refer to as inflation.

The conclusion here is that when dollar prices are rising over time, it is because there is an excess supply of dollars. This is true regardless of whether firms are making profits or whether their profit margins are going up or down.

What Does History Tell Us?

Okay. Okay. Maybe that is a compelling story. But what evidence is there? Well, let’s start with this chart from a paper by George McCandless and Warren Weber in their paper “Some Monetary Facts.” It plots the average inflation rate and the average rate of money growth in 110 countries over a 30-year period. Such graphs are common in intermediate macroeconomic textbooks (such as Robert Barro’s Macroeconomics). This certainly seems like evidence in support of the idea that more dollars in circulation means higher dollar prices.

Ah, but maybe this isn’t convincing. This graph cannot tell us about causation. Sure, I’ve told a story about how more dollars in circulation leads to higher dollar prices using basic price theory, but perhaps this neat little story just happens to coincide with a world in which there is a positive correlation that matches my theoretical prediction. Or perhaps higher prices lead to an increase in the demand for money, which leads to more money in circulation. In that case we need another example.

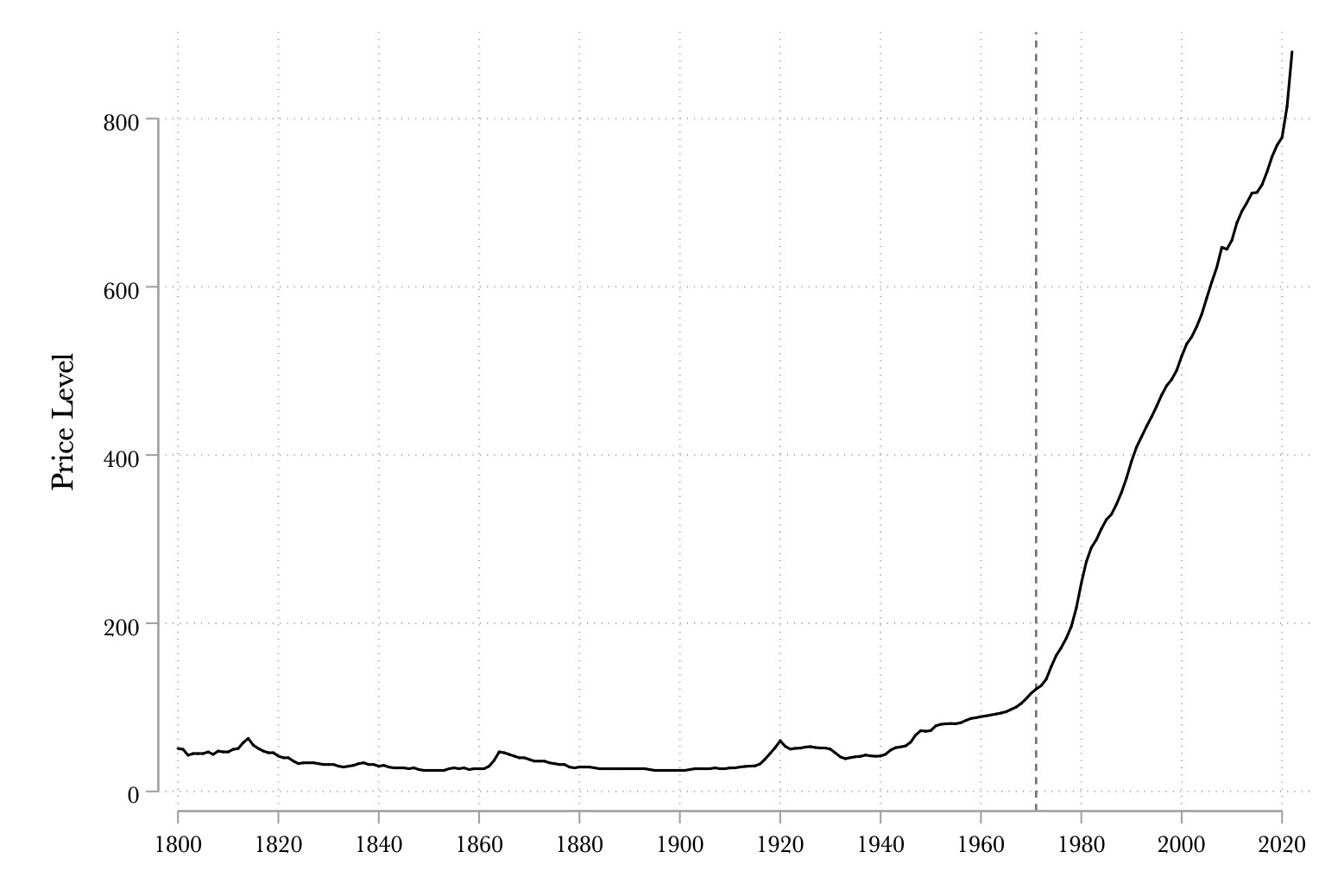

Well, let’s think of another way to test the hypothesis. There were significant changes in the policy regime over the last two centuries. During its early history, the U.S. was on a commodity standard. My model would suggest that dollar prices should be relatively constant under the gold (or silver) standard because dollar prices rise when there is an excess supply of gold (silver). On average, the supply of gold (silver) should rise at a rate equal to economic growth. Most evidence on money demand suggests that money demand is unit elastic. Thus, the demand for gold (silver) should rise at the rate of economic growth as well. On average, dollar prices should be relatively stable. Of course, this isn’t strictly true because the gold standard didn’t operate well following World War I and wasn’t replaced until the new Bretton Woods system was introduced. The Bretton Woods system made the dollar convertible into gold by other central banks. But in 1971, that system was put to an end and replaced with the fiat dollar.

If the story that I told is correct, then one should expect that dollars prices were relatively stable under a commodity standard. Following the collapse of the Bretton Woods system, there is no constraint on the supply of dollars since dollars are no longer redeemable for any commodity and the dollar is no longer defined as a particular quantity of some commodity. Below is a graph of consumer prices using data from the Federal Reserve Bank of Minneapolis.

Note that the predictions of my simple story are consistent with the graph. Stable prices are evident during the days of commodity money. There is modest inflation during the Bretton Woods era and then consumer prices rise rapidly following the collapse of Bretton Woods. The simple story seems consistent with the data again.

The Problem with “Greedflation”

This brings me inevitably back to so-called “greedflation.” This story is an attempt by people to treat every bout of inflation like isolated cases that require the fresh eyes of a new detective. And yet, greedflation has no explanation for the evidence put forth above. Perhaps they could dismiss the first chart as a spurious correlation or reverse causation. However, the same cannot be said of the second. Are we supposed to believe that there was a sudden outbreak of greed that corresponded almost perfectly to the collapse of the Bretton Woods system? Have firm markups vastly exploded in our era relative to other eras?

Even ignoring those questions, the greedflation advocates could argue that I am correct in general, but not in this single instance. However, even this claim is dubious. As I showed in a previous post, even if the only data one had was data on inflation and the growth rate of the money supply at the end of 2020, it was perfectly predictable that we would observe persistently high inflation over the next 2 years. Once again, the simple story that I am telling here is able to predict out-of-sample.

In his famous study of religion, René Girard lamented that “a panic-stricken refusal to glance, even furtively, in the only direction where meaning could still be found dominates our intellectual life.” One can’t help but see a similar refusal in recent discussions of inflation.

You make a good case against “strong greedflation,” the idea that greedy companies are driving our current inflation. But I think there is case for “weak greedflation.” Companies with market power, who can hold prices above the marginal cost of production, act to preserve their margins as supply costs rise. This forces the full impact of tight supply onto other sectors, consumers, labor, and small business. Because large companies (rent collecting) can pass on their full increase in costs, the price adjustment mechanism in the economy is stiffer, making it harder to use slow inflation with government tightening. In my view, “greedflation” is not the cause of rising prices, but it does make inflation more persistent.

Don't we need to look at which products and services had increased prices and by how much? It's possible that firms with high market power took the opportunity to push the envelope on their prices to test the water on demand elasticity.