In Praise of Lumpiness

Nature does make some leaps. And that's good.

Natura non facit saltum. “Nature does not make leaps” goes Alfred Marshall’s line in his Principles of Economics. This idea is now central economics; we, as economists, focus on marginal analysis. Small changes here drive small changes there. We often assume the world (utility and production functions) is smooth, continuous, and twice differentiable, so “small changes” just means a derivative.

When life is not smooth, continuous, and twice differentiable, economists get nervous. First, it makes solving models harder. That’s never fun. I model you can’t solve doesn’t help much. But even if you can still solve the model, things that are not smooth, continuous, and twice differentiable, what I’ll call “lumpiness”, can also generate other problems.

From a technical perspective, the problem is that equilibria might not exist when life is lumpy. If the price per car is less than I’d be willing to pay for 1 car but more than I’d want to pay for 2 cars, how many do I buy? Does that correspond to what sellers are also willing to do? Without smooth curves, what is the equilibrium?

If an equilibrium does not exist, we can’t rest assured that outcomes are efficient. We don’t know what will happen!

Yes. These things do keep me up at night. Generally, economists have done their best to work around lumpiness problems. David Friedman has the easiest workaround in his text.

Sometimes, though, “lumpiness” can be a good thing and actually help people achieve an efficient outcome easier. I want to go through two examples, both having to do with externalities.

Coasean Bargaining

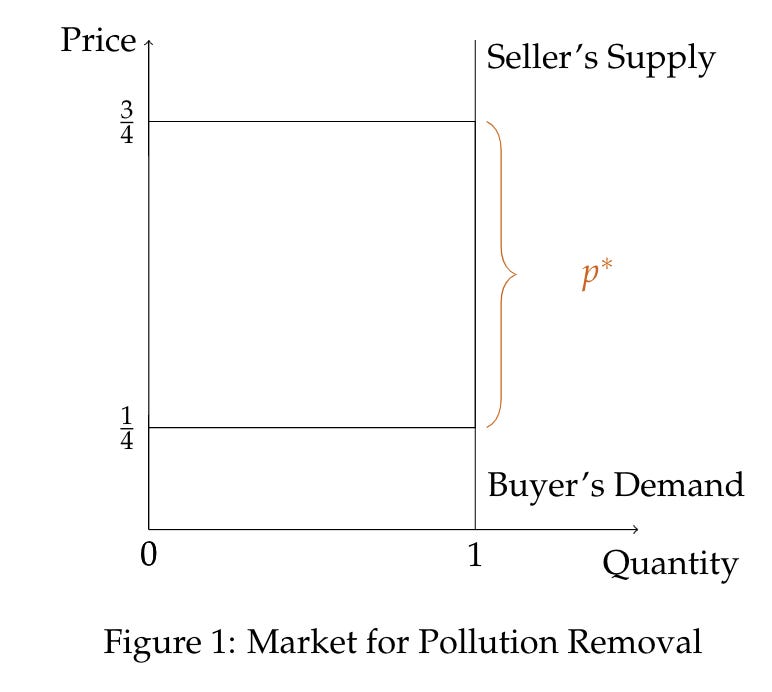

First, think of a classic Coasean bargaining problem. There is a market for pollution removal. The externality hurts one person (who is the demander of pollution removal services) at $3/4 per unit but only the other person can eliminate it (who is the supplier of pollution removal services) at a cost of $1/4 per unit. Suppose now that up to one unit of externality can be eliminated in a continuous fashion (although not differentiable at Q=1… uh oh… anyways, let’s move on).

This market is what’s called a bilateral monopoly and we can draw the mostly-standard supply and demand curve.

If bargaining isn’t really an issue (the zero transaction costs case in Coase) and everyone acts like price-takers, any price between $1/4 and $3/4 will clear the market and an efficient amount of pollution reduction is supplied.

Even though the equilibria are Walrasian (price-taking), they are not perfectly competitive. People should not act like price-takers in this situation, since the Walrasian price is not unique.

If people decide to bargain, we may have the possibility of each siding holding-out for a better price. To see this, suppose the Walrasian price is $1/2. Suppose the supplier decides to only be willing to supply .9. That drives the price up to 1 and is a profitable deviation for the seller. That's what I mean by the original problem is not perfectly competitive.

The seller is withholding part of his supply to gain more favorable terms of trade. We can imagine the demander doing the same. This could lead to a full unraveling of the market. This “hold-out”/bargaining problem is one reason to expect the pollution market to not lead to the efficient level of pollution reduction.

But lumpiness can save the day!

Now suppose pollution prevention can either be installed or not. The quantity traded is 0 or 1. (Note this is closer to the cases in Coase, where there is a simple decision option: eliminate the externality or not.)

While we haven’t fully eliminated the bargaining issue (people still may haggle over the price), things may improve. There is no longer an easy way to capture all the surplus by withholding a bit of the supply, unraveling the market. The restriction on the trade/strategy space improves outcomes, like in a Prisoner's dilemma where the defect option is removed for both people. Tieing our hands can be good.

Inframarginal Vaccine Externalities

For a topical application (wait, not that, I mean an application that is topical), consider the case of a vaccine and its externality. When I get a vaccine, I generate a positive externality by protecting other people. If I could directly choose my “level” of vaccine, it is well-understood that I would not choose the efficient amount. I would consume too little of the vaccine.

But vaccines are basically zero or one. You are vaccinated or you are not. Yes, you could choose to get vaccinated a minute earlier and think of it as being closer to a continuous choice. But let’s suppose it is zero or one.

If the vaccination is a zero/one decision, then one vaccine is the efficient amount and it is the amount I, Brian Albrecht, personally chose. There is an externality, but the outcome is nevertheless efficient. Buchanan and Stubblebine call this type of an externality an “inframarginal externality.”

Yes, my actions affect others. But that doesn’t affect the efficiency. There isn’t an externality on the margin, since the margin is now only zero to one. For policy, I don’t need to be subsidized to reach the efficient amount. Policy just needs to get me over the hump to get it at all, the lump. It does not need to be fine-tuned.

The lumpiness means it easier to achieve the efficient take-up rate of the vaccine. We have a chance at efficiency.

Maybe this is just my half-baked idea. I have yet to work out all the details, but it seems relevant. What economists usually see as frictions/problems may sometimes be exactly what makes life function.

There are lots of interesting ways to complicate these issues. A more sophisticated theory would incorporate that people can sometimes choose the “lumpiness” of goods. I just want to show how what is sometimes seen as a bug is actually a feature.

Thanks to the people who sent newsletter ideas. They were great. I just need more time to do them justice. Keep them coming!