Market Power and the Productivity Slowdown

Market power may not work how people think it works.

For over a decade before the pandemic, the U.S.—really the whole world—experienced a slowdown in productivity growth. In the case of U.S. manufacturing in particular, after decades of robust labor productivity growth, manufacturing productivity in the U.S. hit a ceiling around 2011 and has actually declined in the years since. This slowdown has hit leaders and laggards.

This isn't just a blip—it's a persistent trend that's lasted over a decade. It's particularly puzzling given the rapid technological advancements we've seen in areas like automation, artificial intelligence, and advanced materials. Some economists have suggested that this apparent slowdown might be due to the mismeasurement of productivity in the digital age. However, Chad Syverson provides compelling evidence against this hypothesis, suggesting that the productivity slowdown is indeed real and not merely an artifact of measurement issues. Joey Politano and Noah Smith have both dug into the more granular data. Read both if you want more details on manufacturing.

I want to take a step back and explore the basics of productivity accounting. This will help us understand why one popular meme alone (rising market power) seems unlikely to explain the productivity slowdown.

Warning: There will be math. More troublesome is that much of this will involve accounting. We need to be careful not to reason from these accounting identities. But our explanations must fit these identities, so we cannot ignore them.

Productivity Basics

Let's start with the two main measures of productivity:

Labor Productivity (LP): This is simply output divided by labor input.

Y is output and L is labor input (often measured in hours worked). Adding up total output has complications, but in the scheme of productivity measurements, this is fairly straightforward. In particular, this measure doesn't depend on specifying a production function.

Total Factor Productivity (TFP): This measures the efficiency with which all inputs are used in production. Sometimes it is referred to as multifactor productivity. It's inherently connected to a specific production function. For simplicity, let's use a Cobb-Douglas production function:

\(Y = A * L^α * K^{(1-α)}\)Where A is TFP, K is capital input, and α is the output elasticity of labor (not the labor share - this distinction will be important).

In our Cobb-Douglas world, LP and TFP are related as follows:

Taking logs and then looking at growth rates, we get:

Where gX denotes the growth rate of X.

This equation tells us something crucial: LP growth and TFP growth (gA) can only diverge due to changes in the capital-labor ratio, so-called capital-deepening.

Here, we can already see that, in this simple setup, output market power does not matter for productivity unless it affects A or changes gK-gL. Again, the takeaway is not that the Cobb-Douglas model is true. It’s more meant to give pause on the popular meme that instinctually links the fall in productivity to market power.

Labor Market Power

One possibility is increasing labor market power. Sometimes, it is more accurately referred to as a growing labor market wedge, the wedge between wages and output for a worker. While labor market power is a huge discussion in many areas of economics, it’s often left out of productivity discussions. And that’s a problem. I think it can help us think through possible causes of the manufacturing slowdown. One exception is an old blog by Dietrich Vollrath.

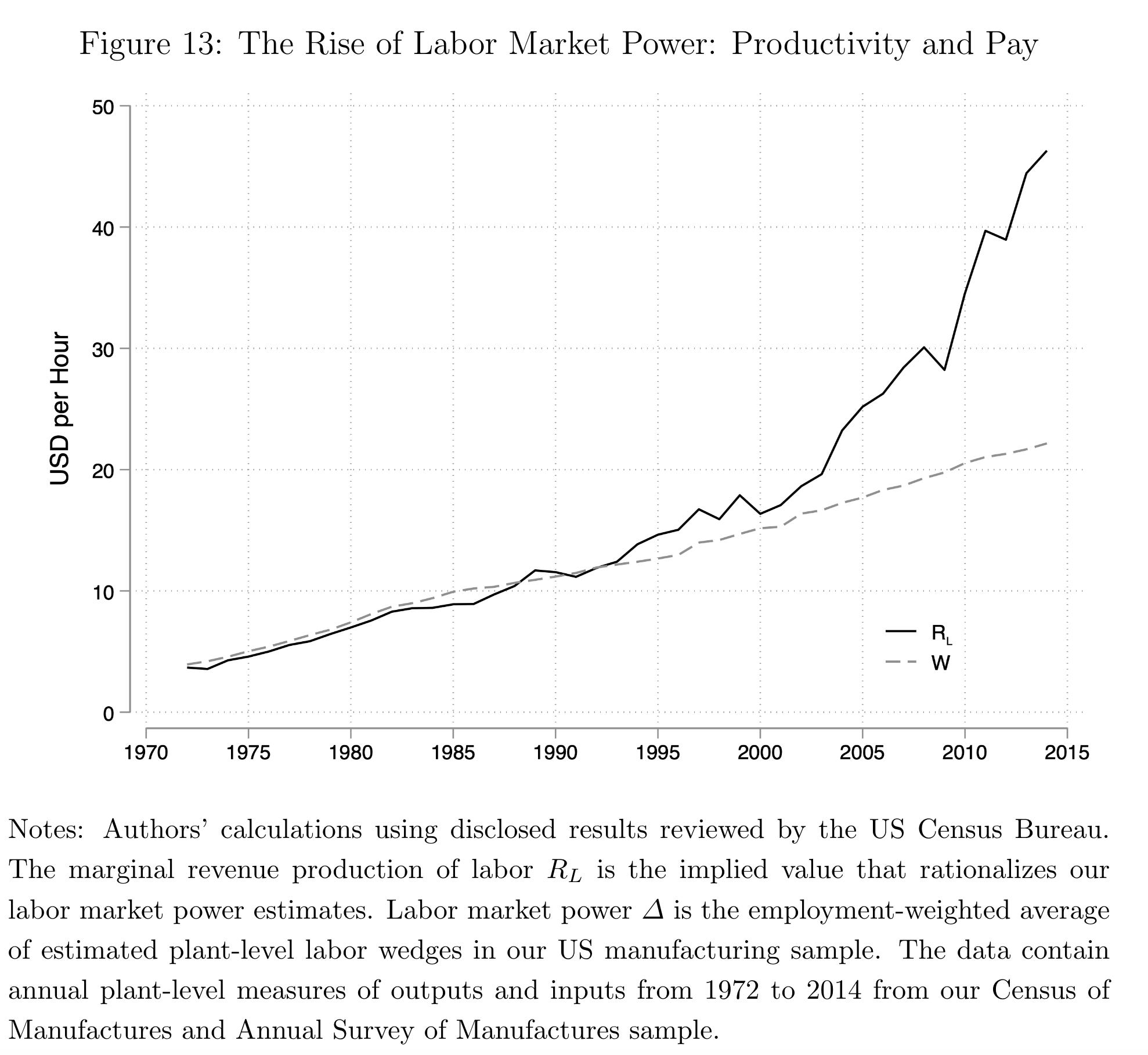

Especially in manufacturing, there is good reason to believe labor market power has increased. Using detailed plant-level data from U.S. manufacturing, Kirov and Traina (2023) document a significant rise in the labor wedge (markdowns) from 1972 to 2014. They estimate that the average markup was around 1 in 1972, suggesting a competitive labor market. But by 2014, it had risen to about 2—implying that workers were producing twice as much as they were being paid.

Crucially, Kirov and Traina find that this rise in markdowns aligns with the timing of the productivity slowdown, with inflection points in the early 1990s and early 2000s, before really taking off around 2010. This timing matches turning points in the manufacturing productivity trends.

However, the connection between labor market power and productivity is not so simple. In our simple model, increasing labor market power should actually increase measured labor productivity. Here's why:

When firms have more power in the labor market, the cost to the firm of hiring a worker, on the margin, rises. If this is confusing, read here.

The firm responds by reducing labor.

This leads to capital deepening—an increase in the capital-labor ratio (K/L).

Remember our equation for labor productivity growth: gLP = gA + (1-α) * (gK - gL). As K/L increases, gK - gL becomes positive, pushing up labor productivity growth.

Moreover, if labor market power is increasing over time, we would expect this effect to compound, leading to accelerating labor productivity growth.

This counter-intuitive idea that labor market power would increase productivity is closely related to the observed uptick in productivity around recessions. If labor supply drops, either due to a recession or increased labor market power, it can manifest as growth in measured labor productivity. Neither of these is usually what we think of as the benefits of productivity growth, but they would show up as labor productivity.

Taken together, market power affects these measures:

Output market power (markups) doesn't directly affect TFP or LP. It affects inputs symmetrically, so it doesn't change the capital-labor ratio (K/L).

Labor market power (markdowns), however, can affect measured LP:

Increased labor market power leads firms to substitute capital for labor.

This increases the capital-labor ratio (K/L).

As a result, measured LP rises, not due to increased technological efficiency but due to input substitution.

Labor Market Power Measurement Issues

I’m being a little fast and loose. This is a newsletter. Forgive me! Many of the productivity measurements assume perfect competition, so we are mixing and matching models.

Let’s now explicitly introduce a measure of labor market power, the markup μ, defined as the ratio of the marginal product of labor to the wage:

This is the gap between the two lines in the Kirov and Traina graph. In a perfectly competitive market, μ = 1, so wages equal marginal product of labor, ∂Y/∂L. But if firms have market power over labor, μ > 1. The presence of a markup drives a wedge between the marginal product of labor and the wage.

I’ve already said mismeasurement is an unlikely explanation for the slowdown. But let’s think through which way the mismeasurement would go.

The key measurement problem arises because we typically don't observe true output elasticities (α). Instead, we use observed factor shares. With labor market power, there's a wedge between the true output elasticity of labor (α) and the observed labor share (sL):

Here is where we need to be careful about how the measurements actually work. Up to this point, I assumed the economist observed the level of labor. That’s not true in most cases. In most cases, the economist observes the payment to labor. Moreover, the capital share is taken to be whatever is left over after paying labor. This isn’t a problem for labor productivity because Y and L are both (in principle) measures of quantities, not revenue.

In practice, the growth rate of measured TFP (gAm)—m for “measured” A—becomes:

Which we can rewrite as:

The gap between true gA and measured gAm is a bias.

But a bias is not enough to explain a slowdown. The bias above is about the level of productivity. For the bias to be a mismeasurement to generate a slowdown, the bias needs to be increasing over time that bias is increasing.

The key insight here is that if there's a markup (μ > 1), and if labor is growing slower than capital (gL < gK), then measured TFP growth will be lower than true TFP growth. Moreover, if the markup is increasing over time or the gap between the growth of labor and the growth of capital increases, this divergence will worsen.

In other words, growing labor market power, a labor growth slowdown, a capital growth increase, or any combination of those three can make it seem like TFP is growing more slowly.

Now, let's return to our puzzle. Both LP and TFP growth have slowed significantly since around 2011. Can labor market power explain this?

If it were just increasing labor market power:

Measured TFP growth would slow or even decline due to the bias we've identified. We have observed a decrease in TFP.

But LP growth should increase due to capital deepening (firms substituting capital for labor).

We don't observe this uptick in labor productivity. Both measures are slowing. This suggests that while labor market power may be increasing, it is unlikely to be the sole or even primary driver of the productivity slowdown. The simultaneous slowdown in both TFP and LP growth points to a more fundamental change in productivity dynamics. We need to look for factors that could be suppressing true productivity growth across the board.

Again, this is a super simple exercise. There are more complicated models that can fit rising market power and falling productivity. Also, I’m just assuming market power rises. Why? What’s the cause? This is reasoning from identities. The key takeaway isn’t that the slowdown cannot be about market power. Instead, it is more about noticing that the relationship between market power and productivity is more complex than often assumed. While increasing labor market power may be happening, it alone seems unable to explain the observed productivity slowdown. In fact, in our simple model, it should have the opposite effect on labor productivity.

Again, price theory can serve as an antidote to oversimplified narratives.