People act. Markets clear. Everything else is commentary.

The basic elements of economic models

The goal of Economic Forces is pretty simple: help people (readers and writers alike) avoid saying dumb things about how markets work. There's a lot of confusion out there about prices, inflation, competition, market power, and basically everything happening in the economy.

But there's a second goal too, in service of the first: help people avoid saying dumb things about economics (the field) itself. The field gets criticized for all sorts of things —some fair, many not. Sometimes these critiques reveal more confusion about how economists use models than actual problems with economics.

Today’s newsletter tackles both goals by breaking down what economic models actually do.

First, let me acknowledge that economic models are weird things. Most people don’t spend their days building simplified versions of reality and arguing about which simplifications matter. But that’s exactly what many economists do. We draw curves, write equations nobody will solve in real life, and make assumptions that sound ridiculous (“assume everyone knows everything”). Then we claim these clearly unrealistic models tell us something useful about reality.

I get why this seems absurd. But models aren't trying to capture everything; they’re tools for thinking systematically about how markets work. Understanding how economists build and use these tools helps reveal what's really happening in the economy.

Most of the confusions I see stem from mixing up two distinct pieces of any economic model. Let’s break them down.

Every standard economic model has two conceptually distinct parts:

Behavioral conditions: These specify how each agent (person, firm, etc.) behaves given their constraints. For example, in many models we assume consumers maximize their utility subject to their budget constraints and firms maximize profits.

Equilibrium conditions: These specify how individual choices fit together. The most common equilibrium condition is market clearing—quantity supplied equals quantity demanded. This is where lots of “physical” constraints come in. People can’t consume apples that are not produced or don’t fall from the tree. This is should just be called a “solution concept,” as I explain more below. I like that because equilibrium can be very dynamic and changing in modern economic models, so equilibrium may give the wrong impression.

Think of a model like a play: the behavioral conditions are like the script telling each actor what to do, while the equilibrium conditions are like the stage directions ensuring everyone ends up in the right place at the right time. Both are needed. If you change the stage directions, you change the play.

Here’s where people often get confused: They mix up behavioral assumptions (like price-taking) with equilibrium conditions (like market clearing).

Behavior vs. Equilibrium Across Different Models

Let’s look at some examples to see the difference.

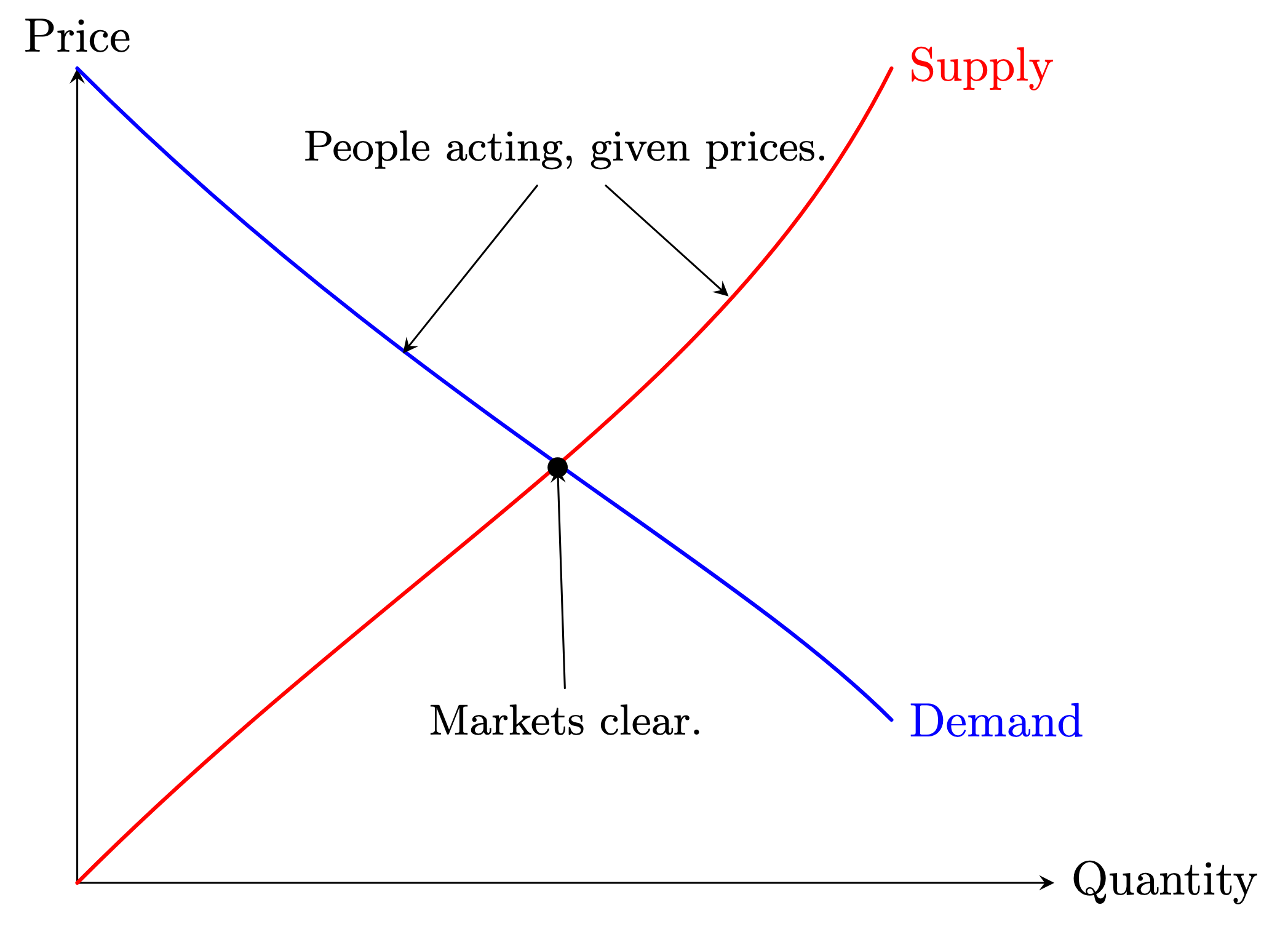

In a standard Walrasian or Marshallian market model, buyers and sellers maximize their goals and take prices as given—they’re “price-takers.” These are two behavioral assumptions. People in the model assume (rightly or wrongly) that they cannot affect prices in anyway and do the best they can given that constraint. From those assumptions, we draw a demand curve which tells us the demander’s decision for any possible price and the same for suppliers.

There’s a separate condition which is about how all the people in the model fit together. This market clearing condition is separate—it’s the equilibrium condition that makes sure everyone’s choices are compatible. We need to be on both the demand curve and the supply curve at the same time. That’s the X. If we have price controls, we aren’t at the intersection. It’s a different set of behavioral assumptions and equilibrium conditions.

But we can tweak those conditions one by one. Take the classic monopoly model. The monopolist isn’t a price-taker—they choose price strategically knowing how demand responds. That’s a different behavioral assumption. But looks like market clearing here since they—in effect—choose a market-clearing price. Why wouldn’t they? If they set price too high, they’d have unsold inventory. Too low, they’d have unfilled orders. It maybe looks like the monopolist chooses the equilibrium but its still helpful to separate the parts so we can think of them one by one. It’s an equilibrium, even if we are no longer on both the supply curve, just on the demand curve.

But we could easily change the model again to break that tight connection between setting prices and market clearing. Consider the two price setters in the Bertrand model of competition that I’ve written about before. With identical products and costs, competition drives them to price at marginal cost. The outcome looks like perfect competition even though the behavioral assumptions are totally different. And, again, no one chooses the equilibrium.

Finally, take game theory models with Nash equilibrium. Here the behavioral assumption is that players maximize given their beliefs about what others will do. The beliefs are like the beliefs in a Walrasian model about prices being constant. The equilibrium condition is not traditional market clearing. Instead, the condition is that these beliefs are correct.

For example, in a two-player static prisoners’ dilemma, we have each player choosing cooperate or defect subject to their beliefs. By assumption, punching the cops and running out is not something the players believe is possible, just as buyers may not believe they can affect the price of the good. In the prisoners’ dillema, the beliefs do not really matter since defecting is the best option no matter what the other player does. In jargon, defect is a dominant strategy. Here the specific equilibrium concept isn’t that important since any reasonable equilibrium will point to defect, defect as the outcome. But we don’t know that before writing down the model, so it’s better to be explicit.

Adding Time

Unlike the prisoners’ dilemma, the exact equilibrium concept used can matter a lot when we add time. Time makes beliefs about the future relevant. Unfortunately, time also breaks our need divide between behavior and equilibrium.

Consider the classic cobweb model of agricultural markets. Farmers must plant crops months before selling them, so they have to base production decisions on their expectations of future prices.

The behavioral assumption in the cobweb model is that farmers use today’s price as their prediction of future prices—what economists call “naive expectations.” That seems on par with the price-taker expecting the price to be fixed no matter the quantity purchased. The equilibrium condition is still market clearing—supply equals demand when the harvest actually comes to market. But unlike standard neoclassical models, this period’s equilibrium price affects next period’s supply through farmers’ expectations.

This seemingly small change in timing creates interesting dynamics. High corn prices this year lead farmers to plant more, increasing next year’s supply and pushing prices down. Low prices then cause farmers to cut back planting, reducing supply and driving prices back up the following year. The process repeats, creating cycles that can either converge to a stable price or persist indefinitely.

But dynamic models in economics today often takes a different approach. The behavioral assumption remains that agents maximize their expected profits or utility. But what beliefs do they have about the future? Instead of saying the future will be like today, we say what the people will do for each belief they have. Again, this is no different from the price-taker model where we show what happens for each price (even prices that never occurred).

Out of the vast array of possible beliefs and actions, what's do we say will happen? What's the solution to the model? What changes is the equilibrium condition: we require that expectations match what actually happens in equilibrium. This “rational expectations” condition ensures nobody makes systematic forecasting errors.

There's too much to say about rational expectations for one newsletter but I'd say it's not really about perfect foresight by the agents in the model but about how the market must clear somehow and the economist needs a tool to pin that outcome down, just as they need to know where the supply and demand curves cross to say will happen.

The Rationality Red Herring

Once we’ve separated out the behavioral conditions from the equilibrium conditions, we have a language for building but also critiquing models. Critics of economics often focus their fire on the rationality assumption—the idea that people optimize their choices given constraints. “Nobody actually solves complex optimization problems!” they cry. “People make mistakes, have emotions, follow rules of thumb!”

But this misses a crucial point: many key predictions of economic models don’t actually depend much on rationality at all. Think about what Becker did in his 1962 paper.

If you're so smart, why aren't you someone in an economics model?

You are reading Economic Forces, a free weekly newsletter on economics, especially price theory, without the politics. Economic Forces arrives weekly in the inboxes of 5,500 subscribers. You can support our newsletter by sharing this free post or becoming a paid subscriber:

He imagined people making completely random choices about what to buy, subject only to their budget constraint. When the price of a good increases, the budget constraint rotates, becoming steeper. Even with random behavior, this rotation of the budget line forces people to buy less of the now-more-expensive good on average. Voila—we get downward-sloping demand without any optimization or rationality.

This isn’t just a theoretical curiosity. Gode and Sunder demonstrated the power of budget constraints experimentally with their “zero-intelligence traders.” These computer programs made random bids and offers in a market, constrained only by not being allowed to lose money. Despite their complete lack of strategic thinking, the markets converged near competitive equilibrium prices and allocations. The budget constraint did all the work.

Why does this matter? Because it suggests some critiques of economic models are focused on the wrong thing. Whether people perfectly optimize their utility functions is far less important than the fact that they can’t spend more than they have. The budget constraint binds regardless of how thoughtfully or randomly people make their choices.

We can sometimes change the behavioral assumptions and keep the predictions.

This idea shows up again and again. As Armen Alchian pointed out in his 1950 paper, market outcomes often follow patterns we’d expect from “rational” behavior even if individual decision-makers are far from perfectly rational. What drives these patterns? The brutal logic of survival and market clearing.

Consider a simple example: firms that consistently price above their competitors while offering identical products will eventually lose all their customers and go out of business. This prediction doesn’t require assuming managers are rational optimizers—it just requires that customers tend to prefer paying less for the same thing and that firms that lose money eventually shut down. Here, the equilibrium condition of market survival does the heavy lifting, not assumptions about managerial decision-making.

None of this means the rationality assumption is worthless, as I argued in the linked Becker piece above. It remains useful for deriving precise predictions and understanding individual choices. But it does suggest we should be more focused on understanding the institutional structures and equilibrium conditions that shape market outcomes. Those often matter more than exactly how “rational” individual decision-makers are.

The Equilibrium Red Herring

Another common confusion comes from the word “equilibrium” itself. The term conjures images of stillness, like a ball resting at the bottom of a bowl. This leads critics to claim economic models can't capture real-world dynamism since they rely on “equilibrium.”

But this misunderstands what equilibrium means in economics. Equilibrium isn't about things being static; it’s about having conditions that help us predict what will happen. Yes, everyone is acting, but we need to a way to sort out all the possible outcomes into some that are more likely than others. Sometimes those conditions predict constant, unchanging outcomes. But often they predict patterns of change.

Consider financial markets. An equilibrium condition might say no one can make risk-free profits through arbitrage. This doesn’t mean prices stay fixed - quite the opposite! It means prices constantly adjust to reflect new information. The equilibrium prediction is one of perpetual change, a random walk.

Sometimes our equilibrium conditions don’t even give us a unique prediction. Game theory models often have multiple equilibria, different possible outcomes that could each be stable. That’s not ideal but if that’s the best we can do that’s the best we can do. The equilibrium conditions still help us understand what outcomes are possible and maybe what factors determine which one occurs.

The key is that “equilibrium” just means we have enough conditions to analyze what happens in our model. It’s about having a complete framework for prediction, not about predicting stasis. Markets can be constantly churning while still following equilibrium patterns of change.

Market Clearing Beyond Price Adjustments

So far we’ve mostly talked about markets clearing through price changes. But equilibrium conditions can work through other channels too, especially when prices can't adjust freely.

Take price controls. If the government caps gas prices below the market-clearing level, excess demand doesn't just vanish. The market still has to “clear” somehow. Often this happens through queuing - people wait in long lines to buy gas at the controlled price. The time cost of waiting effectively raises the total price until demand matches the available supply. The behavioral assumption about how much gas people want to buy hasn’t changed. What's different is the equilibrium condition - instead of price adjustments bringing supply and demand together, time spent waiting in line does the job.

Quality adjustments offer another way markets can clear when prices are sticky. Consider rent-controlled apartments. Landlords who can't raise rents to market levels often let maintenance slide instead. The effective price stays below the official cap, but tenants get lower quality housing. Again, the behavioral conditions haven't changed much - tenants still want housing and landlords still want profit. But the equilibrium happens through quality degradation rather than price increases.

Airlines show both forces at work. When flights are overbooked, we see both queuing (standby lists) and quality adjustments (worse seats, longer layovers). The market still clears - everyone eventually gets where they're going or gives up trying. But the adjustment happens through non-price channels.

This highlights something important: equilibrium conditions are about making choices compatible, not about reaching some idealized outcome. Markets will clear one way or another. Understanding the channels through which clearing happens - whether through prices, waiting times, quality changes, or something else - often matters more than the specific behavioral assumptions we make about individual choices.

Learning from Real Market Outcomes

So far I’ve been thinking about the model as what we are studying and what different models say. But we really care about the world out the window. The framework of behavioral assumptions versus equilibrium conditions isn’t just useful for understanding economic models—it helps us interpret real-world market outcomes. When we observe something puzzling in markets, it’s often because we’re focusing on only one piece of the puzzle.

Take soft drinks. Coca-Cola’s secret recipe seems to give it significant market power—a behavioral advantage that should let it charge higher prices than competitors. Yet we typically see Coke and Pepsi priced identically. This suggests something important about the equilibrium conditions in the market. Despite product differentiation, the threat of losing market share to rivals appears to constrain pricing behavior. The observed outcome tells us more about how the market actually clears than what we might guess just from looking at Coke’s apparent advantages.

Or consider industries where we see persistent excess capacity—firms maintaining more production ability than they regularly use. This might seem irrational given the behavioral assumption that firms maximize profits. But viewed through the lens of equilibrium conditions, excess capacity starts to make sense. Take inventories. At first glance, keeping excess inventory seems to violate the behavioral assumption that firms maximize profits. Why tie up capital in unsold goods? But Alchian showed that inventories serve a crucial role in market clearing by reducing information and search costs. Inventories allow firms to handle unpredictable fluctuations in demand without constantly adjusting prices. As he explains using the example of a newsboy, trying to perfectly match supply to daily demand fluctuations would require either costly instant price changes or leaving some customers unserved.

This helps explain why we observe apparently “inefficient” practices like retailers maintaining buffer stocks. The equilibrium condition isn’t just about matching supply and demand in a static sense—it’s about minimizing the total costs of trade, including the costs of finding trading partners and negotiating terms. Inventories emerge as an efficient market response to these information frictions.

At the same time, stocks could could serve as a credible threat against potential entrants, helping establish an equilibrium where new firms choose not to enter despite apparently profitable opportunities. I’m not saying we know in advance the role, but the framework helps us think through what is going on.

The key insight is that when we observe market outcomes that don’t match our initial intuition, we should ask whether we’ve properly understood both the behavioral incentives and the equilibrium conditions at play. Are firms responding to competitive pressures we haven’t considered? Are there institutional features affecting how markets clear? Real-world observations can reveal equilibrium conditions that might not be obvious from just studying individual firm behavior.

This perspective reminds us that economics isn’t just about building theoretical models—it’s about understanding how actual markets work. The distinction between behavioral assumptions and equilibrium conditions gives us a powerful tool for making sense of what we observe in the real world.

The point is that these pieces serve different roles in our models. Behavioral assumptions tell us how individuals act given their constraints. Equilibrium conditions ensure all these individual choices fit together consistently.

Next time you see an economic model, try breaking it down this way:

What are the behavioral assumptions for each type of agent?

What conditions ensure their choices are mutually compatible?

This framework helps clarify what different models are actually assuming and how they work. It also shows how models that seem quite different (like perfect competition vs monopoly) can share some common elements while differing on others.

Of course, real markets are more complex than our models. But understanding these building blocks helps us think more clearly about how markets work and what assumptions we’re making when we model them.

Great stuff. I think it's an uncanny valley problem. Suppose you were modeling animal behaviour. How would a bear behave if he were trying to hit a calorie optimum as a function of energy expended and food consumed. This may be a good model of actual bear behaviour or it might not be. But I doubt you'd get criticisms along the lines of bears are just dumb animals they don't do math. But when considering human behaviour the natural reaction is: this isn't how I make my decisions, so the model and any of it's conclusions are irrelevant regardless of model fit.

Read Ran Spiegler’s new book on the “The Curious Culture of Economic Theory” , Ch 8. There is a “engineering” branch of economics call mechanism design which as evolved into market design that starts with behavioral assumptions but has nothing to do with equilibrium.