Has Inequality Risen?

Probably. But probably less than you think.

You are reading Economic Forces, a free weekly newsletter on economics, especially price theory, without the politics. Economic Forces arrives weekly in the inboxes of over 11,000 subscribers. You can support our newsletter by sharing this free post or becoming a paid subscriber:

If there is one popular narrative, one policy-related topic that has dominated economic discourse for the decade that I’ve been actively involved in, it’s inequality.

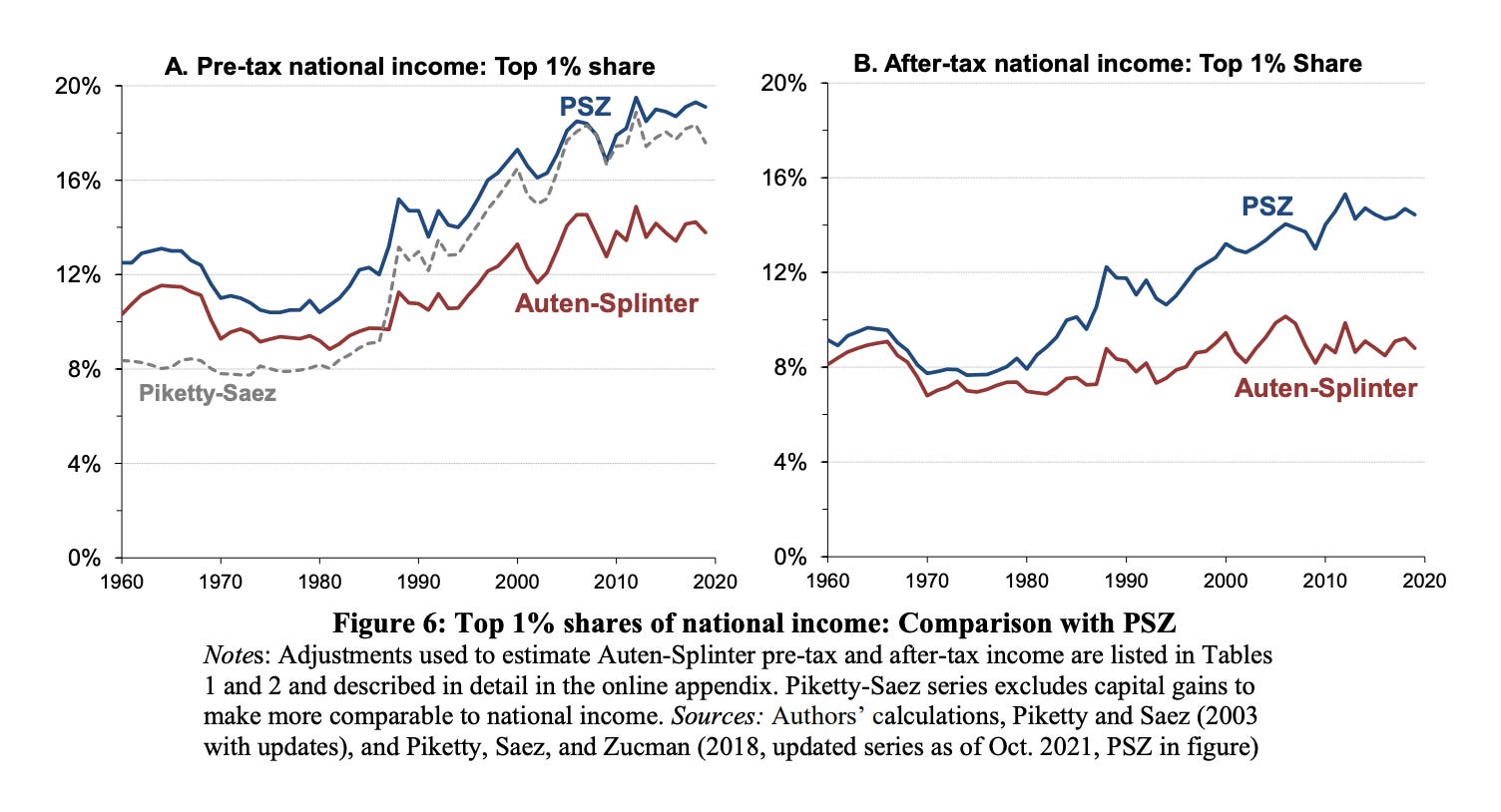

Piketty’s tome came out in 2013, and the shadow remains. Looking at income inequality (compared to wealth inequality), Thomas Piketty, Emmanuel Saez, and Gabriel Zucman’s 2018 Quarterly Journal of Economics article is probably the most well-known in the land of journal articles, building on earlier work from Piketty and Saez (2003). The central takeaway from these authors and what drove the popular narrative was that inequality in the United States had been rising dramatically since the 1960s, especially when we look at the top of the distribution.

As with any headline-grabbing narrative, it may be too good (in the headline sense) to be true. YEARS AGO, we’re talking 6-7 years ago, right as Piketty, Saez, and Zucman came out, Gerald Auten and David Splinter had alternative numbers for the past few decades. Shortly thereafter, Vincent Geloso and Phil Magness pointed out other issues with how Piketty and Saez calculate income shares, especially related to the first half of the 20th century.

So what has happened? Is inequality up or not since the 1960s?

This debate is back in the public discussion after the Auten and Splinter paper was finally accepted at the Journal of Political Economy. Instead of the quick turnaround at for Piketty, Saez, and Zucman at the QJE, Auten and Splinter seem to have gone through the wringer at the journals.

Auten and Splinter argue that income inequality in the United States has not risen nearly as much since the 1960s as Piketty, Saez, and Zucman claimed. Auten and Splinter estimate that the top 1% income share has increased only modestly, from 11.1% in 1962 to 13.8% in 2019. After taxes and transfers, they find almost no change, with the top 1% share rising just 0.2 percentage points

If there weren’t a million headlines about the Piketty et al. numbers, I’d say the more interesting figure is actually about the whole distribution. Their analysis shows significant income growth across the distribution. They estimate after-tax real incomes nearly tripled between 1962 and 2019 for the bottom, middle, and top quintiles. So, their findings are more optimistic than the simple stagnating middle-class narrative we always hear.

Returning to the top 1%, why is there such a discrepancy across major papers in top journals?

Unlike measuring the temperature at a certain location at a certain time, accurately measuring top income shares over long periods proves tricky. A few reasons leave the real experts (compared to the newsletter writers) unsure:

First off, tallying up incomes is a complicated business, especially for the highest income groups. Top earners don't just have simple wage income reported on a W-2. The well-off gain incomes through running businesses, investments, stock options...the whole gamut. These complex sources introduce loads of thorns for researchers. Should we tally income when businesses receive actual payments? How should we handle earnings sheltered from taxes using legal loopholes and creative accounting? Issues pile up regarding reliably estimating missing data when information disappears, or policies change. While such complications infect all economic statistics, these seemingly little details in inequality estimation drive massive swings in concluded trends.

The Weeds of Auten and Splinter

For the nerds, this section goes a bit more into the weeds.

A key reason is that Auten and Splinter develop more comprehensive income measures using additional data sources beyond tax returns. For instance, detailed IRS audit data suggests much less underreported business income goes to top income groups than Piketty, Saez, and Zucman assume based on distributing this income in proportion to reported business income. According to Auten and Splinter, Piketty, Saez, and Zucman also overstate top retirement income shares by treating rollovers between retirement accounts as income when allocating pension fund investment income accruals. (HT: Wojtek Kopczuk for pointing out a previous error. The remaining errors are mine. As I said, this is in the weeds!)

In addition, Auten and Splinter make adjustments to address issues with relying solely on tax return data over long periods. They correct for major tax reforms like the Tax Reform Act of 1986 that changed incentives and income reporting. They also control for the effects of social changes like declining marriage rates, which can artificially inflate top income shares when not properly handled.

Furthermore, Auten and Splinter account for business losses and carryforward losses very differently than Piketty, Saez, and Zucman when allocating underreported income. By ignoring losses, Piketty, Saez, and Zucman essentially take income misreported lower in the distribution and allocate it higher.

Adding that all up, Auten and Splinter find a 6 percentage point lower top 1% pre-tax income share for 2014 compared to Piketty, Saez, and Zucman. About one-third of this difference traces to underreported business income allocation assumptions. The approach has meaningful effects on estimated trends as well.

These methodology improvements allow Auten and Splinter to paint a different picture of inequality changes since the 1960s. They argue past estimates using unadjusted tax return data suffer from various biases affecting both levels and trends.

Newsworthy “facts”

Is Auten and Splinter right? I don’t know. That’s beyond my pay grade.

More importantly, this study is unlikely to be the final word. Estimating income distributions is complex with many uncertainties. Auten and Splinter stress this sensitivity and show alternative assumptions can nudge estimates up or down a few percentage points.

For those of us not directly involved in this research, their paper raises questions about the prevailing wisdom. At a minimum, it highlights how details of methodology and definitions can substantially alter conclusions. It lends credence to other analyses also finding more modest inequality growth in recent decades once using broader income measures.

Instead of giving “the answer,” I think the important part of the paper is that substantial uncertainty remains regarding how much inequality has changed over the past 50+ years. We can't yet make sweeping conclusions about precisely how much - or how little - inequality has actually shifted since the 1960s. The estimates remain foggy.

While the media often trumpets the latest study (inequality-related or not) proclaiming historic changes, the boring truth is the experts can't agree in light of the data limitations. Maybe it’s just t-hacking and what we think are trends aren’t. Even the most careful analyses involve intricate assumptions that could tilt either way.

This phenomenon is more common than just inequality. We see it everywhere within the major economics topics. Markups are rising! (Then point to the study with the most extreme rise). Concentration is rising! (Then point to the study with the most extreme rise).

But as I pointed out before, it’s not beyond the pale to question the presumption. We must. Is concentration rising? It’s asserted everywhere. But some reasonable measures (such as including imports) find falling concentration.

Circling back to the central question, is inequality up since the 1960s?

Probably. But the narrative is completely different if we are talking a doubling of the top income share (as Piketty and Saez suggest) vs. a 0.2% increase. Again, the important part isn’t the exact answer or the particular paper. We need to be comfortable with uncertainty. I guess I’m saying, “Stay away from newspaper headlines; read Economic Forces.”

I'll never forget a study that the Urban Institute made about 10 years ago. It froze the constituents in the base and tracked them over something like 10 years. It found that the upper middle class had made more progress. However, it also showed that people made progress through the quintiles. So, individuals in general do not remain where they were they make progress. The media loves to ignore good news, people seem to like to believe the worst about people, especially if they make more money.

Do researchers have some smart way of imputing the cash-income equivalent of non-cash transfers? Say the government spends $X subsidizing my education or housing or whatever. If that substitutes $X of my consumption, clearly that should count as $X additional income on my part. But presumably in most cases it will substitute some smaller amount of spending and should thus count as some smaller amount of income. This seems like a tricky problem to me.