Stop blaming rising egg prices on market power

High prices may be market power but rising prices are a different beast.

You are reading Economic Forces, a free weekly newsletter on economics, especially price theory, without the politics. Economic Forces arrives weekly in the inboxes of over 17,000 subscribers. You can support our newsletter by sharing this free post or becoming a paid subscriber:

Egg prices are in the news again. Policy responses will likely follow. But not all policy responses make sense.

FTC Commissioner Alvaro Bedoya recently highlighted empty egg shelves and skyrocketing prices, calling for an investigation into potential market manipulation. While his concerns about the egg industry’s supply chain deserve attention, basic economics suggest a simpler explanation may account for much of what we’re seeing.

Bedoya’s argument relies on two main points:

Egg production didn’t drop that much, and

Profits have increased dramatically at major producers like Cal-Maine Foods

The stuff on consolidation is a red herring, as I’ve written many times. So I’ll set that aside. Neither of these (at this point) provides an argument for anything problematic in the market for eggs.

The Supply Side

The data shows this isn’t a small disruption. More than 30 million chickens—roughly 10% of the nation’s egg-laying population—have been killed in just the last three months to prevent disease spread. The total impact of avian flu has been staggering, with more than 136 million birds lost since 2022. The industry has to rebuild from a base of around 318 million birds, roughly one chicken per American.

But nothing in economics says large price changes require large reductions in supply. The size of the price change depends on both supply AND demand elasticities, which are about how easily the quantity supplied and quantity demanded respond to price changes.

In egg production, supply is essentially vertical in the short run due to chicken lifecycles. You can’t instantly produce more eggs when prices rise; you need to raise more chickens first, which takes months. This means even small supply disruptions can generate large price changes.

Eggs are a perfect example of inelastic demand in practice. During the last avian flu go-around, Jayson Lusk wrote a great post. He said that a commonly assumed value for egg demand elasticity is -0.15, meaning a 1% increase in price only reduces quantity demanded by 0.15%.1 Put differently, if the quantity supplied drops by 1%, prices will rise by about 6.67%. In this case, the quantity of eggs dropped around 10%, which would generate a 67% increase in prices. Prices have been volatile, so it’s hard to get a true comparison, but prices have about doubled over the past year. That’s not far off the crude estimate.

This makes intuitive sense when you think about how people use eggs. They’re a dietary staple that’s difficult to substitute. You can’t easily switch to another product when making an omelet or baking a cake. Restaurants with egg-heavy breakfast menus can’t quickly overhaul their offerings. And since eggs are typically a small part of a household’s total food budget, price changes may not drive large consumption changes. When demand is inelastic like this, it takes bigger price increases to reduce the quantity demanded enough to match the lower supply.

Think about your Econ 101 graphs. With a vertical supply curve, any leftward shift of supply (from avian flu losses) results in the same quantity reduction but potentially huge price increases. This isn’t evidence of market manipulation but exactly what we expect to see in competitive markets with highly inelastic short-run supply.

Price Swings Do Not Mean Market Power

There’s an impulse to believe massive price swings must reflect market power. I said “swings.” That’s not accurate. Only massive price hikes get blamed on market power. Price cuts don’t get attributed to cost savings being passed through by a monopolist.

There’s also a tendency to conflate high prices with rising prices when discussing market power. A firm with market power will typically charge high prices, but that doesn’t mean price increases indicate existing market power.

Conversely, firms in perfectly competitive markets may see dramatic price increases when faced with supply disruptions or demand spikes. The egg market illustrates this perfectly - we see rapidly rising prices but that tells us nothing definitive about market power. We need to look at price levels relative to costs, not just price changes, to draw conclusions about competition.

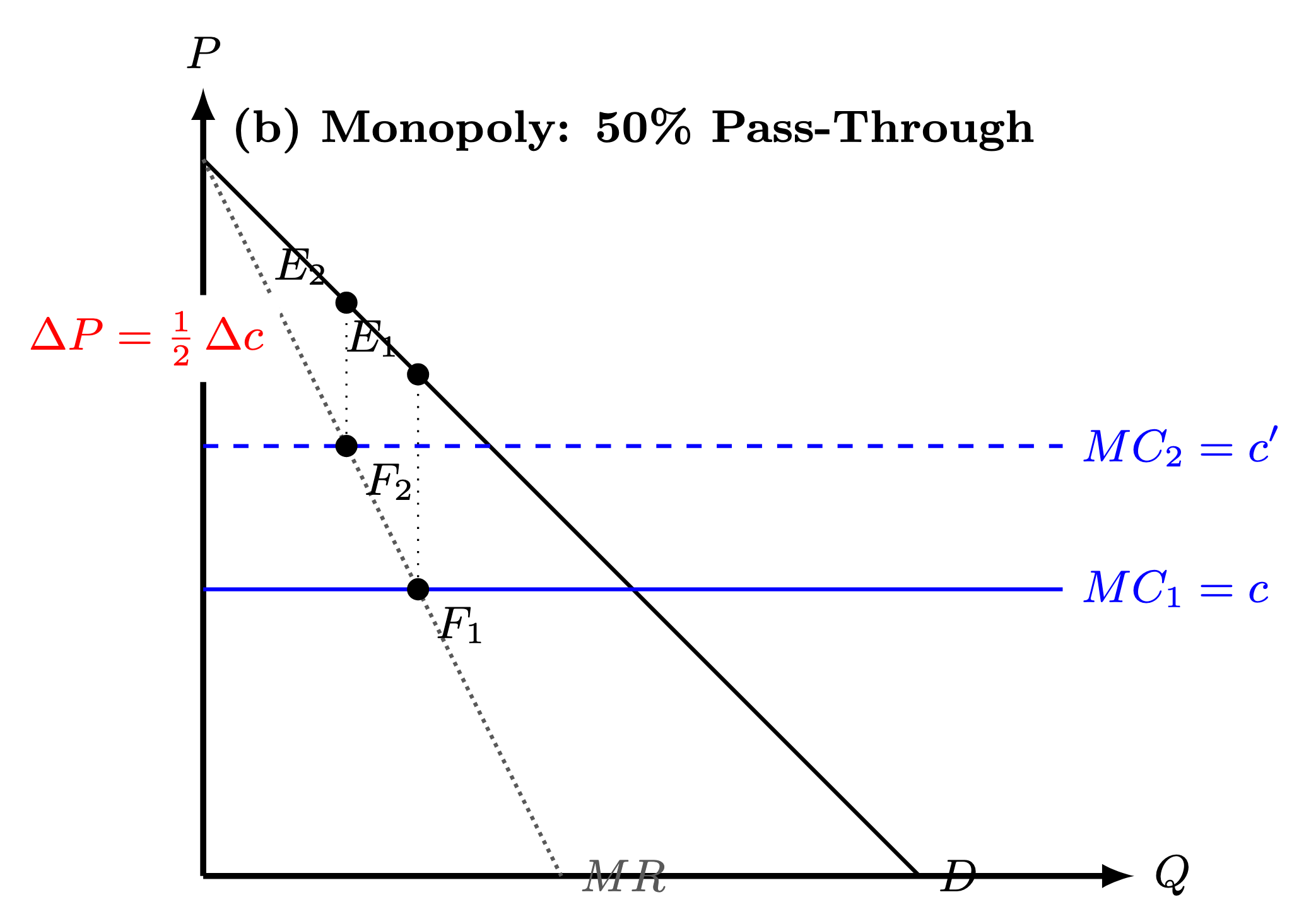

But economic theory suggests swings don’t clearly reflect market power. In fact, competitive markets often show larger cost pass-through than monopolistic ones. For simplicity, let’s assume a linear demand curve and a constant marginal cost curve. These aren’t trivial assumptions but the point is to show the mechanism, not prove it is always true (it isn’t).

With perfect competition and a flat marginal cost curve, you’d see complete pass through.

But if it were a monopoly seller, you’d only see 50% pass-through.

It’s maybe more intuitive to think of a drop in marginal cost and why that isn’t passed through. Marginal revenue drops faster than price. With a linear demand curve, the monopolist’s marginal revenue curve is twice as steep as the demand curve. A $1 decrease in price would mean marginal revenue drops by $2. The monopolist really does not want to pass through that cost saving, which makes more sense. But if the logic applies when moving from c’ to c, it applies exactly opposite if we move from c to c’.

The takeaway here is that even with identical cost changes, market structure significantly impacts how much of that cost increase gets passed on to consumers.

Profits

Bedoya points to Cal-Maine Foods’ dramatic profit increases as evidence of potential market manipulation. While eye-catching, these profit spikes actually tell us less than you might think. To understand why, we need to think carefully about what profits represent in competitive markets.

Think about a simple example: Suppose there are 100 egg producers, and avian flu wipes out 50 of them. The remaining 50, including Cal-Maine, would see their profits soar even in a perfectly competitive market. Why? We already said the price rose, but nothing has happened to Cal-Maine’s costs. Suddenly, they have something scarce—healthy chicken flocks that can still produce eggs when many competitors cannot. That’s not necessarily about anything nefarious.

This connects to a broader point about competition: Under perfect competition, individual firms cannot pass through their own unique cost increases. But when an industry faces a common supply shock, prices will rise together, generating higher profits for firms lucky or skilled enough to maintain production. Again, that’s not evidence of collusion; it’s exactly what we expect in competitive markets, allocating suddenly scarce resources.

As I explained in a previous newsletter on competitive markets, when an industry faces a common cost increase or supply reduction, prices will rise together even without any collusion. This isn’t evidence of failing competition—it’s actually how competitive markets are supposed to work.

While these facts might suggest coordinated supply restriction, they’re also consistent with competitive markets responding to uncertain future disease risks. Current egg production reflects past decisions about chicken investment made under uncertainty about future avian flu outbreaks. The seemingly slow recovery could indicate rational risk management rather than collusion.

Are empty shelves evidence of monopoly?

One aspect of the current situation may cut against market power explanations: the empty shelves themselves. Standard monopoly theory says firms restrict quantity to drive up prices. If producers had significant market power, we’d expect to see high prices WITH eggs on shelves; they’d be maximizing profits by selling at elevated prices, not leaving money on the table with stockouts.

Empty shelves with signs saying “limit one dozen” suggest retailers aren’t letting prices rise enough to clear markets. That’s more consistent with competitive markets under a supply shock than monopolistic behavior.

Importantly, empty shelves also present a puzzle for competitive markets. In a textbook competitive market, prices should adjust to clear the market. However, I’ve argued that we shouldn’t take that literally. Price theory involves a lot more than prices.

The presence of empty shelves, often coupled with purchase limits, strongly suggests that retailers are hesitant to allow prices to fully reflect the magnitude of the supply shock. Eggs are loss leaders to get customers in the store. The grocery store would rather keep prices lower even if it meant empty shelves than to charge higher prices. This retailer behavior implies some force preventing prices from reaching their market-clearing level, whether that friction stems from strategic choices, consumer relations, or other factors beyond a basic supply-and-demand model.

There’s one possible theory I’d like to see someone make:

We need a stronger case for a lack of competition

As I said before, basic price theory is sometimes too flexible—it can rationalize many outcomes after the fact. But competing theories that rely on coordinated behavior or market power are even more flexible, with additional free parameters. When a simpler theory like supply and demand can explain the data, we should be cautious about reaching for more complex explanations.

This doesn’t mean an FTC investigation is unwarranted. The egg industry’s structure and conduct may deserve scrutiny. The FTC has an extremely useful role in studying markets. But if it comes about, we should ground that investigation in careful economic analysis rather than jumping to conclusions from price patterns that could emerge in competitive markets facing supply disruptions.

The antitrust enforcers don’t want to hear this because they’re laser focused on finding market power. However, the core principles of price theory—that prices coordinate decentralized decisions and that common cost changes generate coordinated price movements even without explicit coordination—remain our best starting point for understanding these markets. While market power and anticompetitive conduct are always possible, without a much better case, Occam’s Razor suggests starting with the simplest explanation consistent with the evidence.

The demand elasticity point holds true regardless of whether the market is competitive or a monopoly seller. Whether we’re looking at a perfectly competitive market or one with significant market power, we’re still moving along the same demand curve. A firm with market power might choose a different point on that curve than competitive firms would, but the underlying consumer response to price changes remains the same. This means we can use estimated demand elasticities to understand price-quantity relationships without having to first settle debates about market structure.

Great article Brian. You’ve spoken about perfectly competitive markets and how high profits don’t necessarily indicate market power, as well as the dynamics of monopolies. But what about duopolies? In Australia, our supermarket industry is highly concentrated, with Coles and Woolworths controlling around ~60% of the market. While there are smaller players like Aldi and independent retailers, their market share is much lower, and barriers to entry remain high (in part due to their ability to slash prices to deter competition). It may not be a pure duopoly, but for the sake of discussion, it’s close enough.

There are persistent public accusations of price gouging, yet research (e.g., e61) suggests strong consumer inertia: many shoppers don’t seem to be switching supermarkets even when alternatives exist (possibly implying lack of economising on part of the consumers). But broadly speaking, public frustration is fuelled by a perception that supply constraints have raised costs, which supermarkets are passing down to consumers, yet CEOs are still making multimillion-dollar pay checks -- perhaps implying rising margins. Now, I’m sceptical of the price gouging claims, but I can see why people believe it.

In your view, given this market structure, do sustained high profits in a duopoly primarily reflect true market power, or is consumer behaviour (the inertia I mentioned above) a bigger driver of reduced competitive pressure? I.e. how would you expect pricing dynamics to play out differently in a duopoly compared to a more competitive market?

I have to say, that well generally will put together, this ismissing a lot of important facts. Like calmain being the number one supplier of chicks that lead to layers producing. They almost completely control that market and have near complete control over the supply. They artificially restrict the supply so that they can create these shortages. How does economic theory capture that?

I've heard this argument about economics over and over again in agriculture. About how the consolidation isn't actually manipulative because they look at short-term impacts and say hey it matches economic theory and there's nothing wrong here. It's ridiculous. The evidence is overwhelming to the contrary. Get out of your classroom and get out in the real world and dig deeper. Not implying you don't, but what I'm reading suggest that maybe the case. Please by all means correct me. That's all I ask. I don't disagree with anything you're saying, I'm just saying you're not seeing the whole picture.